Financial Forecasting for Valuation

Financial forecasting of business valuation in the current times is one of the most important skills that a finance professional can bask in because capital allocation decisions are made at pace in the current times. Whether it is to sell a company, raise capital, counsel a merger or construct an internal investment case, your forecast will determine the resultant accuracy and integrity. Valuation is not just a mathematical game but a prospective art that involves an analytical rigour with a sense of good judgment concerning the future performance of an organisation.

In case of junior to mid-level professionals, the interpretation of a financial forecast into the value of the business opens a much more extensive career tool set. It closes the divide between accounting, which is the record of what has happened and strategy, the vision of what might happen. Becoming competent in terms of financial forecasting when it comes to business valuation implies that you can play a significant role in deal rooms, on board presentation, and investor meetings, instead of being a non-agentic number-cruncher.

This paper will take us through the fundamentals, techniques and practical uses of financial forecasting in relation to business valuation. It also discusses the importance of financial statement analysis for business valuation as the most important base on which any plausible forecast should be made. You will come across process frameworks, worked examples and practical advice in the process that will enable you to put these principles into practice in a professional environment with confidence.

The Foundation: Financial Statement Analysis for Business Valuation

A proper interpretation of the business historical performance is a must before a single line of a financial model is constructed. Business valuation analysis includes breaking down the income statement, balance sheet and cash flow statement to determine patterns, anomalies and drivers that will be used to make the forecast. This is not reading in isolation of the numbers they are reading but it is reading about the story behind the numbers in what these numbers say about the operating model of the business, its capital structure and growth path.

Take the example of a middle-sized consumer goods company that is planning to sell to a private equity. The analyst needs to clean up historical earnings by removing one-offs, like legal settlements, restructuring costs, or pandemic-related grants, to get to a clean earnings base before any forecast is prepared. This is often referred to as quality of earnings (QoE) analysis, which makes sure that the forecast has a defensible basis as opposed to the skewed past. This is one of the mistakes that are often overlooked by the less experienced practitioners.

Some of the key metrics used in assessing the business value based on financial statements analysis are growth rates of revenue, trend of the gross margin, EBITDA margin, working capitals cycle and capital expenditure pattern. Both of these are directly fed in to forecast assumptions. When the gross margin of one company has been falling over three years in a row because of increased cost of inputs, a projection of expanding the margin without a strong strategic argument will not be credible – and intelligent buyers or investors will see it.

The Five Core Steps in Building a Valuation-Ready Financial Forecast

A powerful forecasting procedure takes a definite order. Software and templates differ depending on organisations, but the logic is the same. The five key processes that practitioners must consider when developing a financial forecast to use in business valuation are given below.

| Step | Stage | Key Action |

| 1 | Historical Analysis | Normalise 3-5 years of financial results; pinpoint sustainable earnings foundation and drivers. |

| 2 | Assumption Setting | Establish the evidence based revenue growth, margin, capex and working capital assumptions. |

| 3 | Model Construction | Construct combined P&L, cash flow and balance sheet model with interconnected schedules. |

| 4 | Scenario & Sensitivity | Base, upside, downside: Build cases, stress important variables. |

| 5 | Valuation Output | Use DCF, similar company or precedent analysis to come up with value range. |

All of these processes involve a combination of technical skills and professional opinion. Forecasts most frequently go astray of the reality in the assumption-setting stage. New analysts to financial modelling are often too much preoccupied with model mechanics, and underestimate the need to base all assumptions on observable data, be it management guidance, industry standards, or macroeconomic data.

It is notable that financial modeling courses in Singapore have become an established route in the quest by professionals aiming to hone these abilities through systematic education. Topics in these programmes can include integrated model construction, valuation techniques and scenario analysis, which provide participants with both theoretical knowledge and practical experience to create models that stand the test.

Forecasting Methodologies: DCF, Comparables, and the Role of Judgment

The three most common valuation techniques including Discounted Cash Flow (DCF), Comparable Company Analysis (Comps) and Precedent Transaction Analysis are all based on financial forecast to some extent. Knowing how your forecast relates to the valuation method you have selected can guide you in how to focus the greatest analytical attention.

People who do the DCF method are most dependent on the forecast. It is valued by estimating the present value of the future cash flows of the project at a specified time frame, which is commonly five to ten years and discounting such cash flows to the present value, with a weighted average cost of capital (WACC). Even a slight alteration in the terminal growth rate or the discount rate could have a large variation in the results of valuation, and that is why sensitivity tables are an essential tool. An example is a technology company that is generating USD 10 million of free cash flow, which is expected to increase by 15 percent a year and might have a value between USD 120 million and USD 200 million based on the assumptions used about both the WACC and the terminal growth.

Similar company analysis, on the other hand, is more dependent on the existing market multiples as opposed to future projections. But forward-looking multiples like EV/EBITDA on next twelve months (NTM) earnings have to have a solid forecast of the future. This is where financial statement analysis for business valuation analysis directly meets the market-based techniques: as the credibility of the NTM forecast increases, so does the comparability of your multiple. When a business has its forward projections clearly documented with well-reasoned judgments, it will tend to have a narrower multiple range and thus be better defensible.

| Method | Forecast Dependency | Best Used When | Key Risk |

| DCF | Very High (5 -10 yr FCF projections) | Consistent cash flows, extensive history of operation. | Assumption sensitivity |

| Comparable Companies | Moderate (NTM estimates) | Vital M&A market having peer group. | Multiple selection bias |

| Precedent Transactions | Low to Moderate | The last transactions in the domain. | Deal context differences |

Common Challenges and Lessons from the Field

Business valuation financial forecasting is more of an art than science and practitioners are not shy to discuss the pitfalls. Among the most intractable dilemmas is the clash between the natural optimism with the management and the need of the market to be conservative. One of the cases that are well documented in the European retail industry, the target of an acquisition had given five-year forecasts that projected yearly growth of their revenue in the double digit, but its market was shrinking. The financial advisers of the acquirer recreated the forecast with industry data, and the expected growth rate was more than 50 percent lower – and the ultimate acquisition price bore a big mark of that decrease.

The second similar difficulty is the incompleteness or inconsistency of historical data. Especially privately owned companies, their accounting records tend to be in a state of significant clean-up before a meaningful analysis can be undertaken. There can be a misclassification of working capital items, restatement of related party transactions and depreciation policy can be out of a line with industry standards. Recipients of such serious financial modeling courses in Singapore usually discover that the data-cleaning and normalisation stages of a live engagement have little to do with the shiny datasets of instructional practice – an eye-opening but necessary experience.

The third problem is how to inform the non-technical stakeholders of uncertain forecasts. A one-point forecast might be seen by boards, business owners, and even some senior managers as a definite prediction as opposed to a central estimate with plausible alternatives. Presenting the forecast as an interval – and investing in constructed scenario analyses – can be used to manage expectations and results in more informed decision making. The moral of this story is that technical accuracy devoid of a proper message can easily destroy the worth of the most stringent analytical effort.

Process Flow 1: Financial Forecasting Workflow

| Stage 1 | Stage 2 | Stage 3 | Stage 4 | Stage 5 | Stage 6 |

| Data Collection & Cleansing | Historical Normalisation | Assumption Development | Integrated Model Build | Scenario & Sensitivity Testing | Valuation & Reporting |

| 3–5 yrs P&L, BS, CF | Remove one-offs; QoE | Revenue, margin, capex | Linked P&L → BS → CF | Base / Up / Down cases | DCF / Comps / Output |

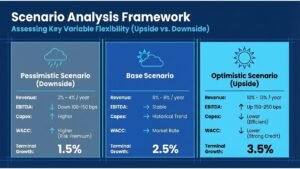

Process Flow 2: Scenario Analysis Framework

| Parameter | Downside Case | Base Case | Upside Case |

| Revenue Growth (Yr 1–3) | 2%–4% p.a. | 6%–8% p.a. | 10%–13% p.a. |

| EBITDA Margin | Compression of 100–150 bps | Stable; modest expansion | Expansion of 150–250 bps |

| Capex (% of Revenue) | Higher; deferred maintenance | In line with history | Lower; efficiency gains |

| WACC | Higher (risk premium) | Market-derived rate | Lower (strong credit) |

| Terminal Growth Rate | 1.5% | 2.5% | 3.5% |

Building Skills and Career Relevance in a Competitive Market

The need to have professionals capable of making plausible financial projections to ascertain the value of a business has been on the rise in investment banking, corporate finance, and in the private equity and management consulting sectors. Organisations are putting more and more pressure on analysts and associates to construct, stress-test, and defend financial models, rather than just populate them. This change implies that basic knowledge is no more, the critical thinking about assumptions and storytelling about the financial background of the numbers is equally regarded.

Structured learning is a factor that can help in closing this gap. The enrolment of financial modeling courses in Singapore has increased significantly over the past few years due to the awareness by the professionals that they need to complement on-the-job training with structured and practical training. The courses are generally a three statement model building through to the DCF valuation model, LBO modelling and the analysis of transactions. They also acquire good modelling practices – logical structure, clear labelling, auditability, and version control – which are as much a part of real-life practice as the mathematics underpinning.

As an active person who is working on developing his/her expertise, it is also important to be able to work on financial statement analysis as a business valuation as a separate skill. Critical reading of financial statements, including identifying accounting decisions, red flags, and comparing with peers, is a skill which can substantially be enhanced through intentional practice. Attempts to study actual company filings, case competitions, or involvement in live transaction work with more experienced practitioners all hastens the acquisition of this analytical intuition.

Conclusion: Actionable Insights for Finance Professionals

Financial forecasting is at the core of business valuation and those who master it have competitive advantage that lasts in many and varied careers in finance. It takes more than technical dexterity in the field, it takes intellectual honesty, the capacity to challenge assumptions, and the communication skills to be able to put complex analysis into straightforward, practical conclusions. Individuals in the initial or middle part of their careers should consider investing time to develop these capabilities as it will pay off in all the positions they will occupy.

Concrete actions to be taken in the near term are a few. First, formulate a methodical line of analysis of financial statements to business valuation by going through the annual reports of listed companies of the industry(s) that you are interested in. Pay attention to the causes of the changes in revenues and margins instead of reading the numbers that are reported. Second, create a library of financial models – begin with a clean three statement model and then to DCF and scenario analysis models. The most effective way of developing true competence is by reproduction of models not by utilizing templates.

Third, in case your company lacks formal training, think of outside programmes. In Singapore, financial modeling courses provide a well-known, practical path to the development and evidence of technical competence. A large number of them are tailored towards working professionals and have flexible formats. Fourth, and, possibly, most importantly, practise the ability to express your assumptions and findings. The difference is the power to articulate why you have predicted a certain rate of growth in revenue not how you have computed that.

Finally, financial forecasting towards business valuation is not aimed at such a goal that would give an accurate picture of the future, it is impossible. It is aimed at building a well-thought-out, clear image of what the future might be with a series of well-spelled-out assumptions and utilizing that image to make improved decisions. It is among the most valuable skills in the field of finance, even to professionals who would like to invest in this field.