Indonesia Business Valuation Trends

One of the most attractive investment destinations in Asia is Indonesia. The fourth most populous country in the world, with its GDP always being one of the ten largest in the Asia-Pacific region, offers an extraordinary scale and diverse market. The diversity of businesses that must be subject to thorough business valuation in Indonesia is as broad as commodity-based conglomerates and state-owned businesses, fast-growing digital platforms, and consumer businesses. However, the unique regulatory framework, ownership patterns, market conventions, and macroeconomic dynamics of the country dictate that conventional valuation methods cannot be applied in a mechanistic fashion but must be customized to the country.

The skill to negotiate these local complexities is a real differentiator for finance practitioners in the investment banking, private equity, corporate development, or restructuring advisory practice in Indonesia and the Southeast Asian region, in general. An assumed value established on assumptions imported and replicated in a developed market, such as a risk-free rate, equity risk premium or a similar set of companies that is not representative of the Indonesian market, will yield results that are technically consistent but that will be practically invalid. The need to learn to anchor core business valuation methods to local realities is thus not a mere academic exercise; a precondition to the plausible work of analysis.

The article will assist junior and middle-level finance practitioners in developing a working knowledge of business valuation in Indonesia. It discusses the prevailing methodologies, factors unique to the market which influence their use, real-life examples of best practice and pitfalls, and the professional business valuation courses and frameworks which may expedite the acquisition of skills. All the time, the goal is to convert conceptual knowledge into practical advice that can be of immediate use to those who work on (or are about to work on) Indonesian transactions and advisory work.

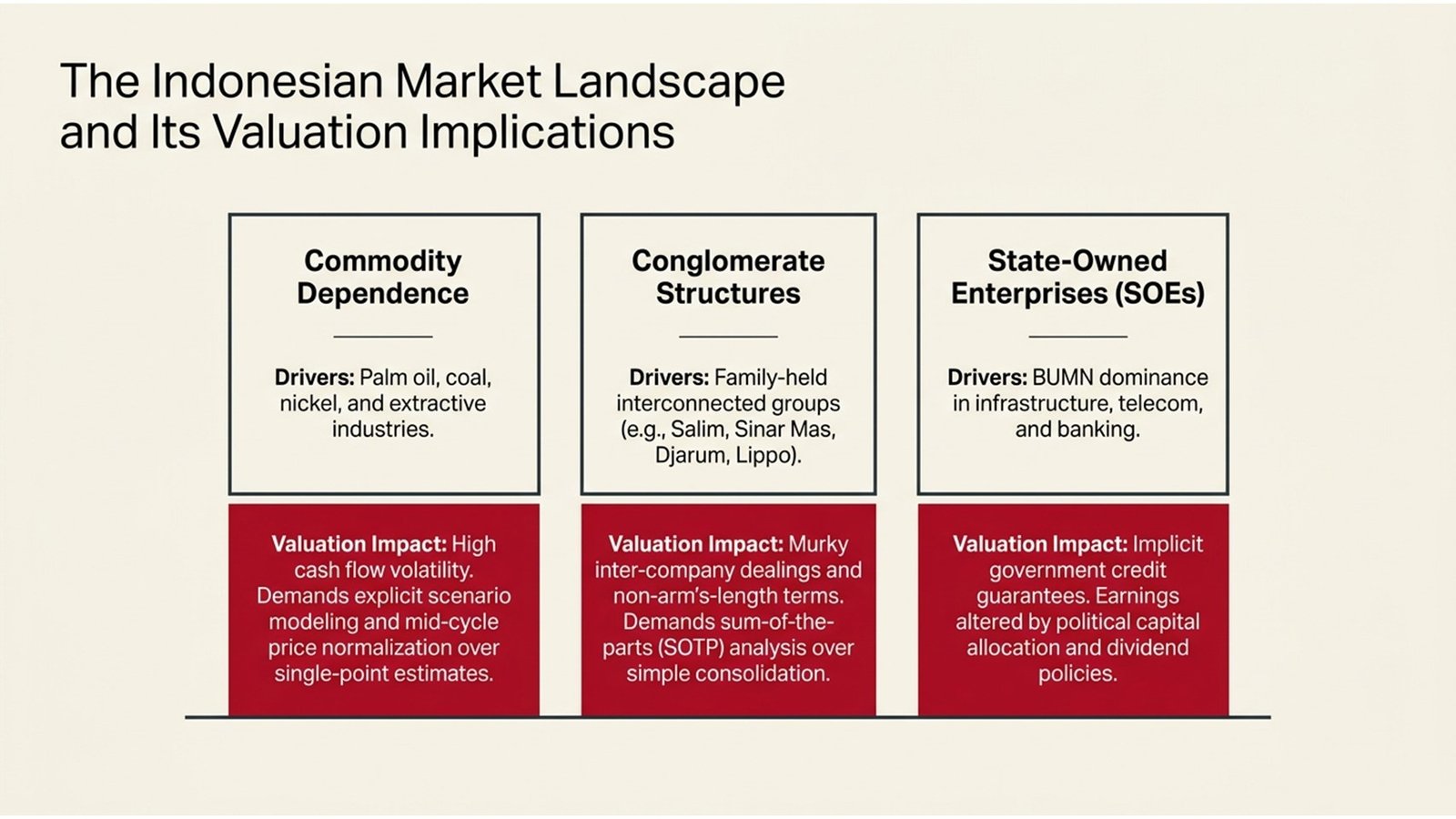

The Indonesian Market Landscape and Its Valuation Implications

Any type of credible business valuation in Indonesia exercise has to commence with a clear picture of the market environment in which the subject company functions in. The economy of Indonesia is typified by a number of structural features, which have direct implications for the financial modelling. The former is commodity dependence: palm oil and coal, nickel and other extractive industries are a disproportionately high portion of corporate income and equity market capitalisation. The cycles in commodity prices create volatility in cash flow forecasts, which cannot be given simple single-point estimates but require explicit modelling of scenarios. What would appear to be a palm oil producer with a high price of palm oil of a given EBITDA multiple will appear radically different when normalised under a mid-cycle price assumption.

The second structure is the existence of conglomerate group structures. The corporate environment in Indonesia is characterised by huge family-held business conglomerates – including the Salim Group, Sinar Mas, Djarum, and Lippo – that have subsidiaries in various industries and are interconnected, through elaborate cross-shareholding arrangements, inter-company dealings, and shared service platforms. A valuation used in one of these groups would involve critical consideration of what terms it is operating on with related parties, the degree to which the reported profitability of the subsidiary represents true stand-alone economics, and whether a sum-of-the-parts or a consolidated approach would be a better way to approach its valuation.

The third characteristic is the presence of state-owned enterprises (SOEs) in the economy. SOEs, also known as Badan Usaha Milik Negara (BUMN), are also prevalent in other sectors such as banking, telecommunications, infrastructure, energy, and logistics, and have listed subsidiaries that are significant sources of market-based valuation standards. There are, however, complexities inherent in SOE valuations: the government ownership can produce implicit guarantees that decrease the perceived credit risk of the business and political considerations can affect strategic choices, capital allocation, and dividend policy in a manner that makes earnings more challenging to predict in a predictable way. This SOE valuation dilemma will be a common theme that professionals undertaking professional business valuation courses, inclined towards the Southeast Asian region, will have to face in the Indonesian context.

Core Business Valuation Approaches in the Indonesian Context

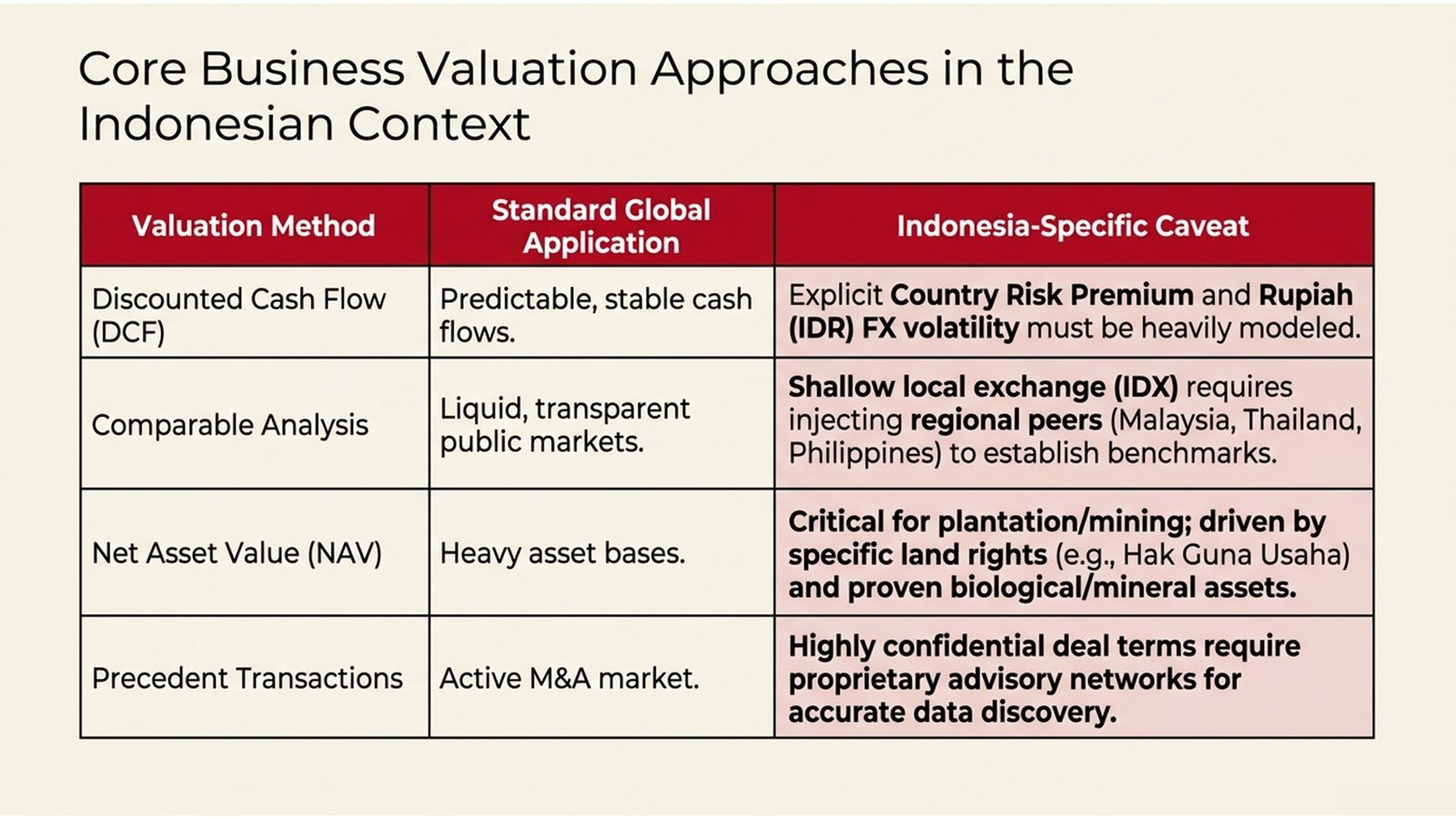

Each of the core business valuation approaches (income-based methods, market-based methods, and asset-based methods) is part of the Indonesian practice, even though the ratio of the weighting between them and the assumptions needed to make them responsibly are significantly different than those of the norms in the developed markets. The discounted cash flow method has been the most popular method of handling transactions of a private company, fairness opinion of a listed company transaction, but it requires special consideration of the discount rate construction. Some agencies have a sovereign credit rating that is lower than investment grade on Indonesia, and the equity risk premium of Indonesian assets has a country risk element that needs to be added explicitly to the standard global equity risk premium when using the models, such as the CAPM.

The market-based methods of analysis, similar to company analysis and precedent transaction analysis, have a practical limitation in Indonesia, which is not as severe as in more developed marketplaces: the superficiality of the local listed equity market. Indonesia Stock Exchange (IDX) has a number of hundreds of companies listed, yet liquidity is concentrated in relatively few large-cap names and most sectors, which would have had a rich pool of listed comparables in the US or Europe, but have few or no in the IDX. Practitioners actively adjust country risk and liquidity differentials by routinely adding country-specific peer IDX comparables of Malaysia, Thailand, the Philippines or Hong Kong. How good the benchmark set is, the results only depend on the care taken in that adjustment process.

The net asset value analysis and the asset-based valuation, in general, are especially important in some sectors of Indonesia. In the case of plantation enterprises, particularly where the pool of biological assets and underlying land rights is large (planted to palm oil or rubber), intrinsic value is often largely driven by the value of the underlying land rights and the pool of biological assets, so a NAV approach would be more informative than a cash flow model based upon the fluctuating prices of volatile commodities. Likewise, in the case of coal mining, the worth of the proven and probable resource base, which has been evaluated by the use of an independent technical report and discounted at a suitable rate of resource risk, is a very important element of any plausible valuation. The summary of the core business valuation strategies and consideration of their use in Indonesia is summarised in Table 1 below.

Table 1: Core Valuation Methods and Their Indonesia-Specific Application

| Valuation Method | Best Applied When | Indonesia-Specific Consideration |

| Discounted Cash Flow (DCF). | Predictable, stable cash flows; long life cycle of investments. | Explicit country risk premium and rupiah volatility should be modelled. |

| Comparable Company Analysis | Peer-to-peer listed; the market is open and transparent. | Light IDX in most industries; local counterparts tended to be required. |

| Precedent Transactions | Vibrant M&A market; similar deals in the market in the recent past. | Terms of deal with: Terms are frequently confidential; they need network and proprietary information. |

| Net Asset Value (NAV). | Businesses having heavy assets: property, plantation, and mining. | Vital in the palm oil, coal, and real estate industries. |

| Dividend Discount Model | Growth pays dividends to companies with a certain policy. | Applicable to banking and utility SOEs in Indonesia. |

Five Steps to Building a Rigorous Indonesian Business Valuation

Regardless of the context, be it an M&A transaction, restructuring, fairness opinion or internal strategic review, a rigorous valuation process is the keystone to plausible analytical work. The five steps given below represent best practice in business valuation Indonesia engagements, and are similar to the frameworks learned in the top professional business valuation programs targeting emerging market and Southeast Asian settings.

Process Flow 1: DCF Valuation Process for an Indonesian Business

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Step 6 |

| Business/Industry Analysis; Review of Regulatory. | Normalise Past Financials (Related-Party Adjustments) | Develop Revenue & Margin Forecasts using Macroe assumptions. | Determine WACC incl. Country Risk Premium & Rupiah Risk. | Calculate Terminal Value; Run Scenario & Sensitivity Analysis. | Cross-Check vs. Comps, NAV and Precedent Transactions. |

Step 1 — Business and Regulatory Analysis. The analyst has to create a comprehensive idea of the business, its position in the market and the regulatory environment that the business is operating in before he or she opens the financial model. In Indonesia, this involves checking the status of the company as to its licensing, its status on the Negative Investment List (where foreign ownership in particular areas is limited), any other applicable regulation by OJK or BKPM, or the terms of any major government contracts or concessions. Such aspects may have a significant impact on the risk profile and buyer universe, and have a direct impact on valuation.

Step 2 — Normalise Historical Financials. Indonesian financial statements, either prepared using the Indonesian Financial Accounting Standards (PSAK) or using the IFRS, often include elements that need close adjustments in order that they can be used as a strong foundation to make future predictions. Some of the most prevalent sources of distortion include related-party transactions reported at non-arm-length terms, one-off gains or losses, and intercompany cost allocations among conglomerate groups. The process of normalisation must be captured in a transparent format since any changes that are undertaken at this point compound in all the other steps of the model.

Step 3 — Build Forecasts with Indonesia-Specific Macro Assumptions. The forecasts of revenue and margin should be pegged to realistic assumptions concerning the Indonesian macroeconomic conditions: the GDP growth trends, inflation rate trends, the rupiah exchange rate trends, the cycles in commodity prices (when applicable) and regulatory changes in the sector. The cost of offshore financing and the currency the revenue and costs will be denominated in should be taken into consideration – a company with USD revenues and IDR costs (or vice versa) has a completely different risk profile than a currency-matched one.

Step 4 — Determine the Discount Rate with Country Risk Adjustment. The WACC of a business in Indonesia should include country risk premium, which is based on political, regulatory, and macroeconomic risks in the Indonesian market. The country risk premium information by Damodaran, which is updated on an annual basis and is commonly used by Indonesian practitioners, gives it a starting point, but analysts should determine whether the company-specific factors should be given an upward or downward correction. Debt cost ought to be based on the Indonesian market borrowing rates, which had been high in the past compared with those of the developed markets, because of the inflation-targeting monetary policy of Bank Indonesia.

Step 5 — Cross-Check and Triangulate. The result of any one methodology will never be a robust valuation. The DCF value must be compared with market-based standards – with IDX comparables and regional counterparts – and, in the case of an NAV analysis or a sum-of-the-parts breakdown. The difference between these methods, and the rational opinion of the analyst as to which part of that range the most justifiable value estimate is, is the essence of the valuation decision. The key assumptions should be transparently given, with sensitivity analysis around the key assumptions, namely the discount rate, terminal growth rate, commodity price and the FX rate to give a range of plausible results.

Real Cases, Challenges, and Lessons Learned

A good example of the complexity of business valuation in Indonesia in the financial services industry is the November 2018-2019 purchase of Bank Danamon Indonesia by the Japanese MUFG. The stepwise purchase of a majority stake by MUFG necessitated negotiating OJK ownership regulations of foreign banks, and structuring the deal within the confines of the Indonesian policy of a single presence, and the assessment of the value of a retail and SME-oriented bank whose quality of loan book and level of provisions were the subject of extensive regulatory attention. The deal demonstrated that regulatory restrictions on ownership structure could cause the theoretical control premium, which is open to a foreign acquirer, to be constrained, something that should be explicitly captured under the valuation framework and not be made away.

The case study of GoTo Group, the merged company between Gojek and Tokopedia, being the first to grow and subsequently go public in the digital economy, offered a precedent of valuing high-growth, loss-making technology companies in an emerging market environment. In April 2022, GoTo listed on the IDX and the valuation frameworks used by analysts and investors to price the company were more typical of US tech IPOs, gross merchandise value multiples, revenue multiples, and unit economics analysis, in an Indonesian regulatory and market structure with little prior experience of businesses of such type. The resultant underperformance of the share price after the listing was indicative of the conflict between growth-based valuation models and the risk tolerance of a majority of people in the local market, more used to value stocks that pay dividends. This case is often used in professional business valuation courses as an illustration of the pitfalls of extrapolating valuation conventions between markets.

The protracted valuation conflicts due to the mining divestment laws of Indonesia, which dictate that foreign holders of some of the mineral resources divest the majority of their ownership in a given number of years of production, have created a valuation experience in the sphere of the constrained ownership interest. The valuation of the world-class Grasberg copper and gold mine had to balance global resource valuation conventions and the individual regulatory limitations on future ownership when Freeport-McMoRan was obliged to sell off 51 per cent of its interest in PT Freeport Indonesia in 2018, which necessitated a transaction that involved significant creative structuring, as well as intensive analytical effort. The moral of the story is that it is impossible to learn about the regulatory architecture of the Indonesian resource extraction without learning how the possessions of this industry are valued.

Table 2: Key Regulatory and Market Factors in Indonesia Business Valuation

| Factor | Valuation Practical Impact |

| POJK Framework (OJK Regulations) | Prepares the disclosure and fairness opinions on transactions of listed companies. |

| Foreign Investment (Negative Investment List) | Limits the universe of buyers; can give discounts on control. |

| Rupiah Exchange Rate Volatility. | Needs clear FX scenario modelling of DCF and returns analysis. |

| Related-Party Transaction Prevalence | Warrants governance discount; this involves close normalisation of financials. |

| Conglomerate Group Structures | The sum-of-the-parts valuation usually proves to be more suitable than consolidated analysis. |

Processes, Due Diligence Challenges, and the M&A Valuation Workflow

The nature of some market-specific challenges that professionals are bound to face and deal with during the due diligence process before a valuation decision is made during an Indonesian M&A deal will define its nature. The quality of financial reporting, which continues to increase with increased use of IFRS-compliant standards by more Indonesian companies and the use of international audit firms, is a mixed bag – especially when it comes to the mid-market businesses and non-listed company universe. Accountants who use unaudited management accounts or accounts prepared by local companies that are not affiliates of international companies must exercise further conservatism in their normalisation adjustments, and in practice, should seek to have independent financial due diligence completed before completing the determination of valuation assumptions.

This is especially significant as part of business valuation in Indonesia: tax due diligence. The tax administration in Indonesia has been more complex and aggressive during the past few years and Direktorat Jenderal Pajak (DJP) is more concerned with transfer pricing compliance, VAT disputes and local tax compliance. A company with past financial records containing aggressive transfer pricing schemes with offshore affiliated parties can have contingent tax liabilities that are neither apparent on the face of the accounts, but can result in a significant decrease in net asset worth. On the same note, the land and building taxes valuations, which are applicable in the property business, plantation and infrastructure business, need to be checked against official records as opposed to management representations.

The due diligence of land rights introduces an additional level of complexity in other sectors such as agriculture, property and infrastructure. The Indonesian land tenure system, with various types of land title such as Hak Guna Usaha (cultivation rights), Hak Guna Bangunan (building rights) and Hak Pakai (use rights), is a system that needs expert legal guidance to navigate and the threat of challenged titles or intrusion by local communities has been a cause of material value destruction in previous deals. The work of valuation analysts who comprehend these risks and who incorporate into their models what can be termed as adequate discounts or contingency provisions is more actionable than models that consider land tenure as a legal side note. The entire M&A due diligence and valuation process of a transaction in Indonesia is shown in Process flow 2 below.

Process Flow 2: M&A Valuation Due Diligence Process in Indonesia

| Phase 1 | Phase 2 | Phase 3 | Phase 4 | Phase 5 |

| Negative List OJK, BKPM, Review Regulatory & Ownership Structure (OJK) | Financial Due Diligence / Accounts normalisation. | Tax Due Diligence (Transfer Pricing, VAT, Local Tax Exposure) | Business- and operations-level DD; ESG and Land Rights Review. | Valuation Synthesis/price negotiation. |

Although there are these challenges, the trend in the financial markets in Indonesia is positive. The OJK has made regulatory advances that have enhanced the use of international financial reporting standards, wider market access to market data via the IDX and other market data providers, like Bloomberg and Refinitiv and the increased involvement of international investment banks and advisory firms have all contributed to creating a more transparent and analytically sophisticated market. The analytical challenges would be invigorating as opposed to prescriptive to professionals who take the time to learn the local structure, not as an emerging high-growth market to be appreciated with an off-the-shelf handbook.

Conclusion: Actionable Insights for Finance Professionals

The size of Indonesia, the trajectory of its development and its structural complexity make it one of the most enlightening and professionally fulfilling markets to do business in terms of valuing business. Those who introduce the most value in this setting are those who have not only mastered the technical aspects of mastering core business valuation approaches, but who are also truly aware of the Indonesian regulatory frameworks, market conventions, and sector dynamics, and who know how and when to localize global methodologies to local realities as opposed to merely being uncritically applied.

There are a number of practical activities that can be identified as effective measures that can be taken by professionals in order to develop or enhance their knowledge. To begin with, become familiar with the Indonesian regulatory landscape since it influences business transactions: the OJK framework of listed company transactions, the BKPM investment licensing regime, the Negative Investment List, as well as the major provisions of the Indonesian Company Law, stipulating minority shareholder rights and the approval of related-party transactions. They are not legal fiddles and bacon but have a direct impact on the valuation frame that is to be employed in relation to a particular transaction. Second, develop a working knowledge of the IDX-traded comparables within the major industries: banking, consumer, telecommunications, plantation, mining, and infrastructure. Being aware of the natural benchmarks of a given asset and what valuation multiples the market uses on them in the cycle is basic knowledge that any analyst can have in conducting a serious business valuation in Indonesia.

Third, a channel in structured learning. Professional business valuation classes which deal with emerging market and Southeast Asian situations – including country risk premium estimation, conglomerate valuation, SOE analysis and commodity-sensitive modelling – will give a framework that will significantly more quickly build to a practical competency than studying by trial and error on live projects. CFA Institute, IVSC (International Valuation Standards Council), and regional finance education programmes with Indonesian content are programmes that may be considered. Fourth, get used to triangulation of valuation inferences to more than one or in more than one methodology instead of anchoring on the output of one model. The art of testing a DCF conclusion with NAV, market multiples, and the implied returns to a potential buyer, is not a good practice in a market in which sometimes data is incomplete, financial reporting is opaque, and regulatory constraints are binding, but it is a vital rigour. It is always these analysts who will develop a lasting credibility in the Indonesian market, as those who do it regularly, and who can explain the rationale behind their valuation range clearly and convincingly.