Applying ESG to Valuation Models

Corporate sustainability and financial performance have become a topic of discussion in academic literature and one of the main concerns of mainstream finance. To an analyst, investor and corporate finance staff, it is no longer a choice of whether or not to incorporate elements of environmental, social and governance in their financial models but rather a requirement of their profession. ESG business valuation models have become at the crossroads of both strict financial analysis and risk assessment, with a prospective view to influence investment decisions, lending, and strategy in the business industry.

This has been precipitated by a set of forces: government regulation that forces companies to disclose climate risks, institutional investors that have introduced ESG screens in their allocation models, and an increasing body of research that suggests that firms with good sustainability characteristics have more resilient earnings and a lower cost of capital in the long run. Training in ESG and sustainable finance has thus since become a top priority among finance departments at banks, private equity firms and corporates alike, as well as professionals who are able to bridge the gaps between ESG data and financial models are becoming more sought after.

The paper aims to assist junior to mid-level finance practitioners to comprehend how to incorporate the ESG into the mainstream valuation models. It reviews some of the most crucial concepts, real-world processes, typical challenges and emerging trends in business valuation that will define the field in the coming decade.

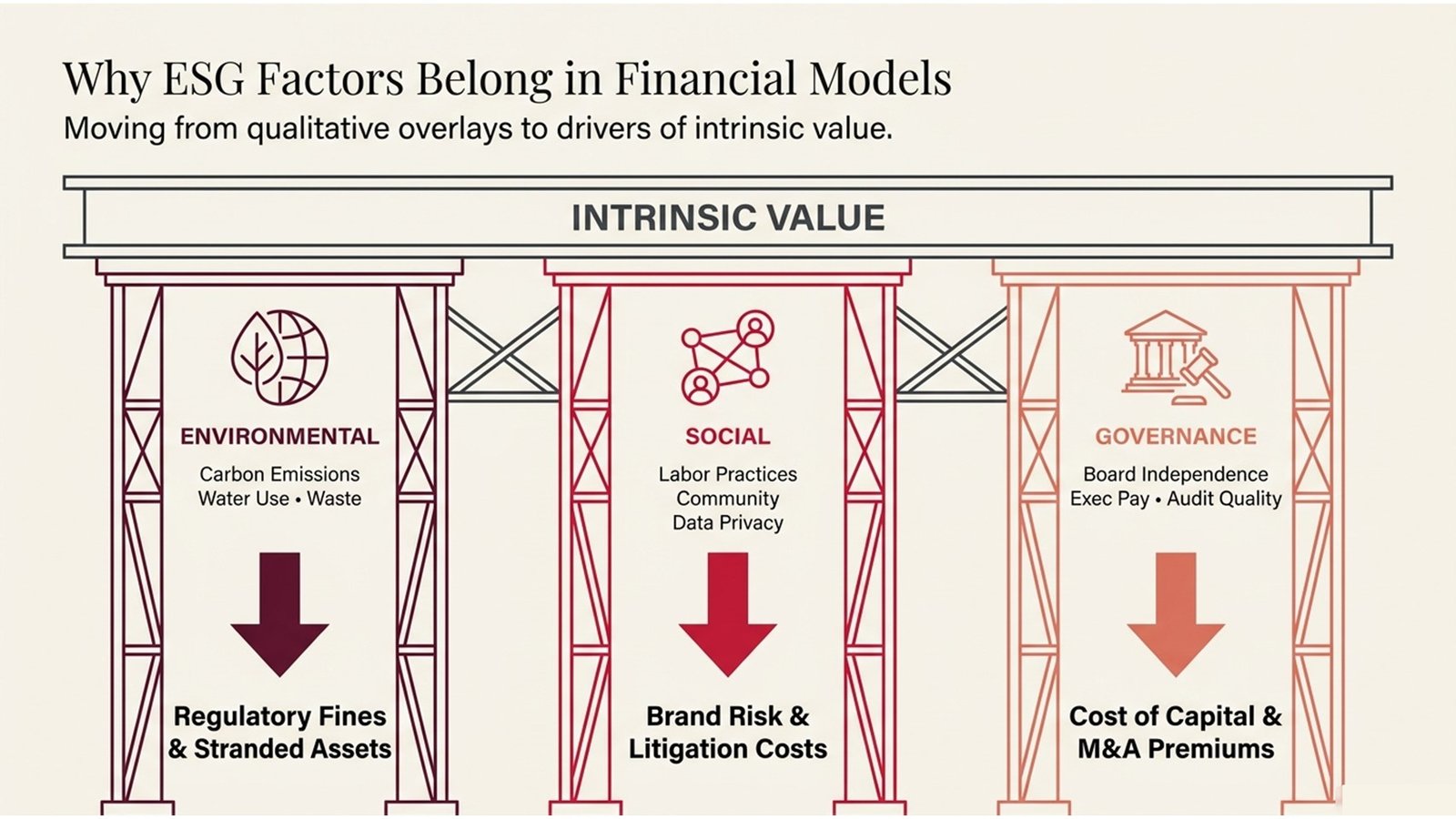

Why ESG Factors Belong in Financial Models

Financial inputs based on audited records and market data that were compiled in the traditional valuation models, discounted cash flow (DCF), comparable company analysis (comps), and precedent transactions, were used to develop the traditional valuation models. By contrast, ESG factors were long considered qualitative overlings, as part of analyst reports, as a footnote and not as a source of intrinsic value. Such a way is growing unacceptable. An example of a climate risk is that it can directly impact the revenue of a company (via regulatory carbon pricing), cost structure (via energy transition capex) and terminal value (via stranded asset exposure).

Take into account the experience of European utility companies during the past ten years. Companies that were heavily dependent on power production through coal were revalued drastically due to the tightening of carbon pricing systems throughout the European Union. Those analysts who had not modeled carbon cost paths to their DCF assumptions were taken by surprise by write-downs, which in retrospect could have been completely predicted. It is not solely an energy-sector tale – it is applicable to any sector with substantial environmental externalities, such as agriculture, mining, shipping, and manufacturers of consumer goods.

There are social and governance considerations that have real financial implications. Unethical labour practices may lead to disruption of the supply chain, boycotts by consumers and legal expenses. Weak governance frameworks are those that are characterised by concentrated ownership, a lack of independence in the board, and/or hidden related-party transactions that are always linked with increased costs of equity capital and reduced M&A values. Anyone in the ESG business valuation models has the task of transforming these qualitative observations into quantified adjustments to enhance the accuracy and strength of financial forecasts.

Table 1 below summarises the three ESG pillars and their primary valuation touchpoints:

| ESG Pillar | Example Factors | Valuation Impact |

| Environmental | Carbon emission, water consumption, wastes. | Fines and regulatory, stranded assets, capex uplift. |

| Social | Work practices, social responsibility, and information privacy. | Brand risk, litigation costs, talent retention |

| Governance | Board independence, executive pay, audit quality | Cost of capital, M&A premium/discount, trust of the investors. |

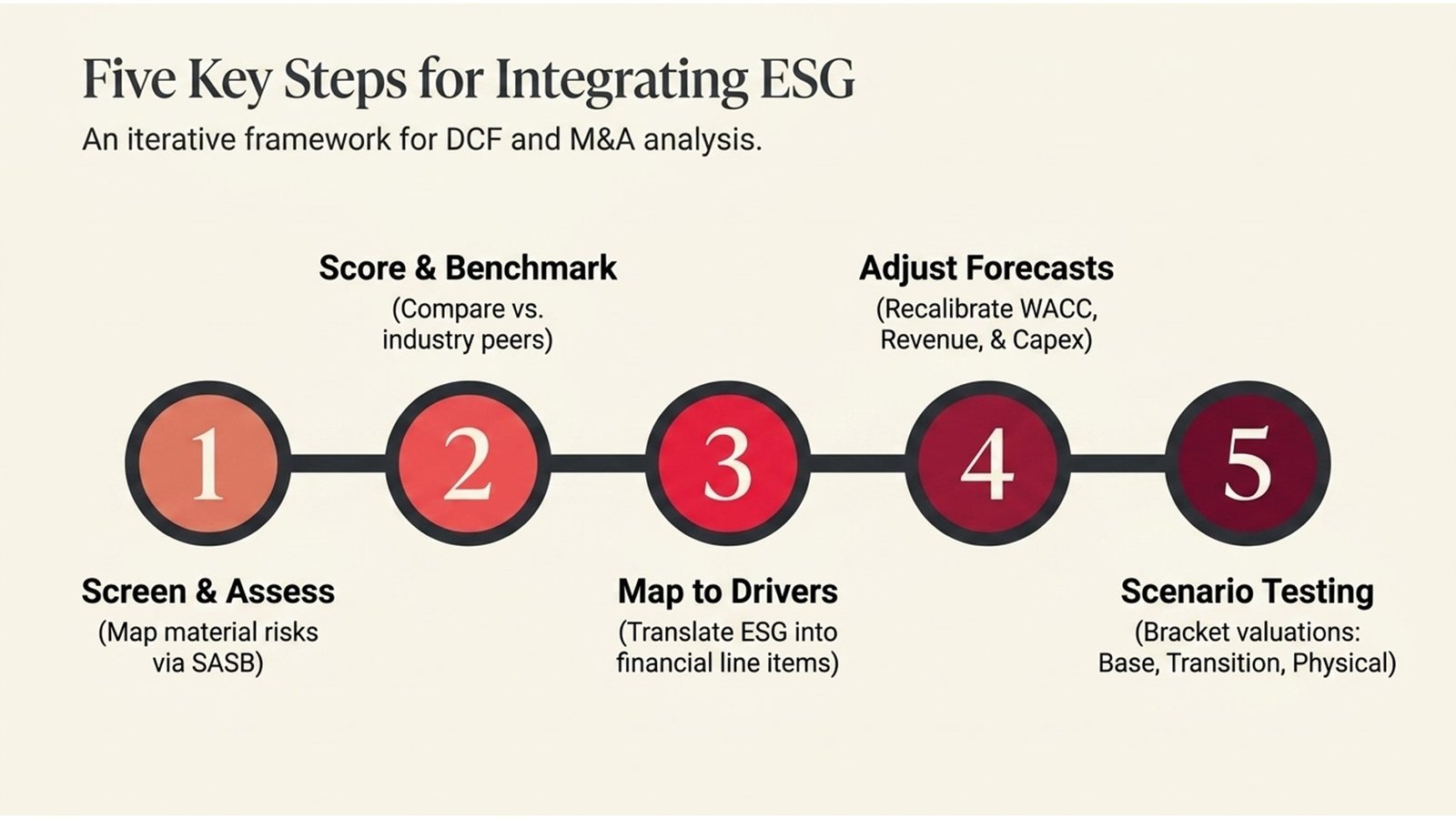

Five Key Steps for Integrating ESG into a Valuation Model

Making ESG a part of a valuation model is not a one-time event but an analytical process. The five steps below offer a useful guideline that can be utilized in DCF analysis, credit ratings, and due diligence in an M&A. The steps are based on the best practice in ESG and sustainable finance training programmes, and are aligned with frameworks by the CFA Institute, Sustainability Accounting Standard Board (SASB), and the Task Force on Climate-related Financial Disclosures (TCFD).

Process Flow 1: ESG Integration into a DCF Valuation

| Step 1 | Step 2 | Step 3 | Step 4 | Step 5 | Step 6 |

| ESG Screening / Materiality Assessment. | Score & Benchmark vs. industry Peers. | Map ESG Financing Risk to Financial Drivers. | Make Revenue, Costs & Capex Forecasts. | Re-set WACC / Discount rate. | Scenario Analysis & Sensitivity Testing. |

Step 1 — ESG Screening and Materiality Assessment. Not all ESG factors have a financial materiality in all companies. The ESG risks faced by a steel producer are quite different from those of a software business. The initial point to start with is to determine the most probable ESG issues that have a quantifiable effect on future cash flows of the company under valuation. The Materiality Map by SASB is a handy reference tool, in that it classifies ESG factors that are industry-specific based on their potential to impact financial performance.

Step 2 — Score and Benchmark Against Industry Peers. After identifying the material factors, the analyst is supposed to evaluate the performance of the company as compared to that of its peers. Third-party ESG data providers (such as MSCI, Sustainalytics and Bloomberg) release scores that may be used as a baseline, but should not be blindly accepted by the analysts. The scores of ESG among providers differ greatly and require further research, such as reviewing the sustainability reports of the company, its regulatory reports, and third-party audits.

Step 3 — Map ESG Risks to Financial Drivers. This is the technical step that is most challenging. It involves the analyst making qualitative adjustments of the ESG observations to individual financial line items. Carbon risk, e.g., could be as a cost adjustment (greater energy cost or carbon permit cost), capital expenditure (investment in decarbonisation technology) or revenue headwind (loss of customers with their own scope 3 emission targets). Social risks associated with labour turnover could be in terms of increased wage expenses or reduced productivity assumptions.

Step 4 — Adjust Forecasts and Recalibrate the Discount Rate. After mapping environmental, social and economic factors to financial drivers, the projections of revenue, cost and capex in the model can be scaled accordingly. Individually, the discount rate, which is the weighted average cost of capital (WACC), should be re-examined. Firms that have higher ESG profiles are likely to have access to less expensive capital; those that have higher ESG risk should receive higher equity risk premiums. There are those who apply a separate ESG risk premium of between 50-200 basis points to the WACC of poor sustainability companies.

Step 5 — Scenario Analysis and Sensitivity Testing. ESG risks are uncertain in nature. There is a high degree of variation in the carbon pricing paths, regulatory schedules and consumer behavior. The scenario approach, involving the modelling of a base case, transition risk scenario and physical risk scenario, enables the analyst to bracket a set of plausible valuations as opposed to bracketing on a single point estimate. This practice is in line with TCFD suggestions and is getting more and more demanded by institutional investors, as well as credit committees.

Real-World Examples and Lessons Learned

The practical application of ESG business valuation models can be informative, which transcends theoretical models. The case of Ørsted, the Danish energy company formerly called DONG Energy, is often mentioned as one of the most convincing examples of successful strategic change that is based on ESG. After selling nearly all its fossil fuel holdings in 2017-2020, Ørsted re-established itself as an offshore wind leader worldwide. Analysts who factored in the transition plan of the company into their valuation models (by modifying their revenue mix projections, assumptions on capital allocation, and regulatory risk factors) would have gotten a huge re-rating that would not have been detected at all by generic DCF models pegged to historical financials.

Another learning experience is the ESG integration process by KKR in the private equity environment. After implementing a formal ESG due diligence framework, the company started to conduct a systematic evaluation of the exposure of portfolio companies to climate risk, social controversy, and governance deficiency at the stage of deal origination. This exercise has allowed KKR to avoid a number of transactions that had a latent ESG liability – such as costs to remediate the environment and supply chain compliance risks that were not evident in the financial statements at the time. The company predicts that ESG due diligence has helped in quantifiable EBITDA growth of the portfolio companies due to the operational efficiency gains associated with energy and resource management.

One of these warning stories is based in the fast fashion industry. A number of international retailers that intensively grew in the 2010s without strong supply chain ESG controls experienced considerable financial impact when factory safety scandals, as well as claims of exploitative labour methods, resulted in consumer and regulatory reaction. To analysts that had not factored in a supply chain social risk of the growth of revenues and made no discount to valuations to governance of extended supply networks, the resulting revenue decline and costs of litigation were a real modelling failure. These instances highlight the need to move past the checklist compliance approach to ESG and sustainable finance training and build real analytical insight.

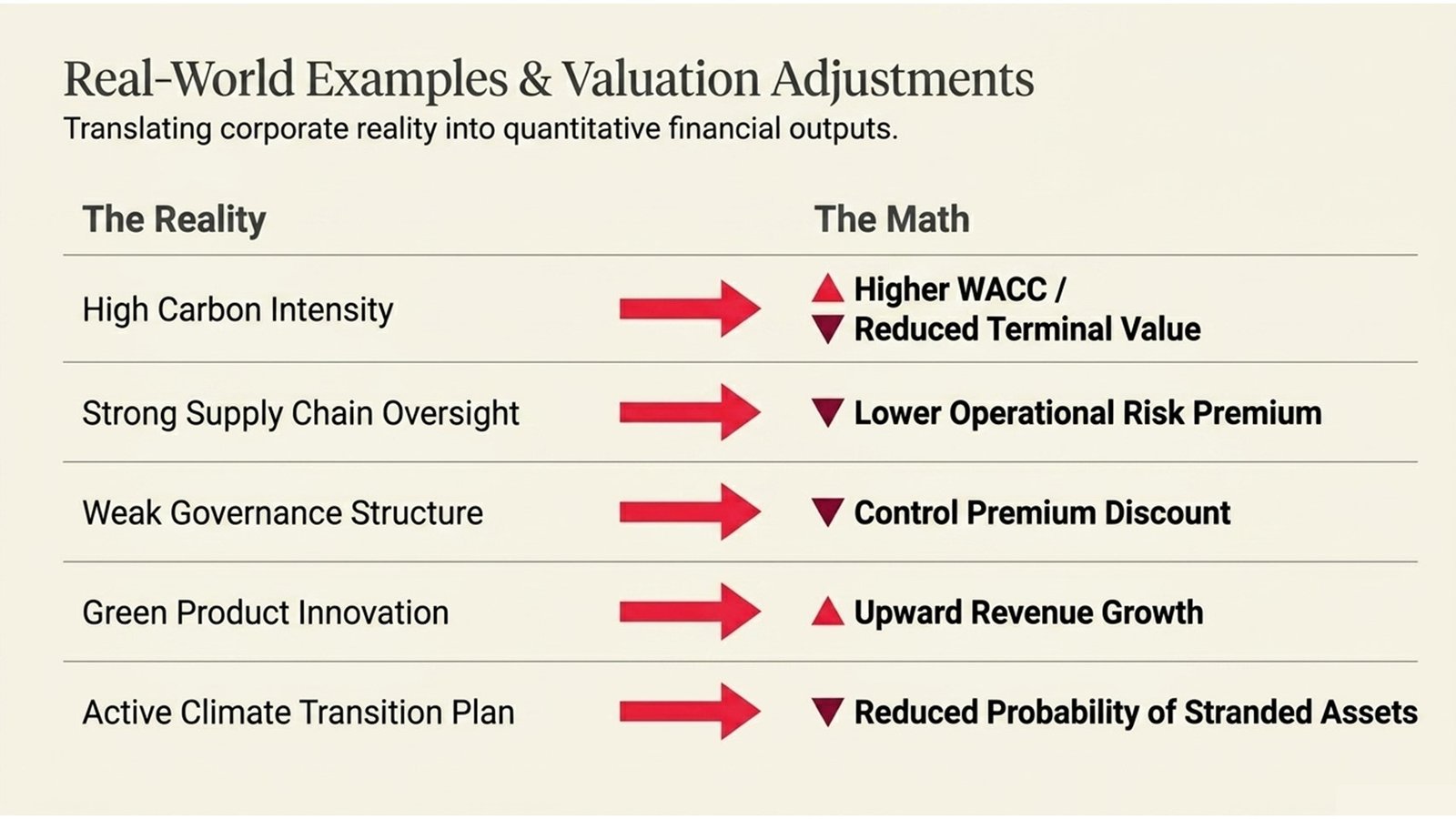

Table 2 below maps common ESG risk factors to their corresponding valuation adjustments:

| ESG Risk / Opportunity | Valuation Adjustment |

| High carbon intensity | Increased WACC; the terminal value is decreased. |

| Well-developed supply chain ESG management. | Reduced the risk premium of the operation. |

| Agency / weak governance. | Control premium discount; increased rate of discount. |

| Innovation pipeline of green products. | Adjustment in the upward revenue growth. |

| Active climate change plan. | Less likely to have stranded assets. |

Processes, Challenges, and How to Overcome Them

There exist several challenges that are well-documented in implementing an ESG valuation process in practice. The most often referred to is data quality. ESG disclosures are not reported consistently, are not fully standardised and are highly variable across third parties (when compared to audited financial accounts). Carbon emissions data of a company can only be released on a scope 1 and 2 basis, but not the more significant scope 3 (value chain) emissions. Some companies voluntarily disclose social measures like employee turnover, pay equity ratio and injury rates, whereas others do not do so. This puts an unbalanced playing field in the analysis.

The second significant issue is that ESG scores have to be translated into financial adjustments. Even when ESG information is at hand, to translate an environmental rating of 45 out of 100 into a particular correction to the WACC, or to make a change to revenue growth, judgment and industry experience are needed. No standardized approach exists and this implies that the business valuation models of ESG that are generated by various analysts on the same company may differ significantly. It is not necessarily an issue, but financial modelling always includes some form of judgment, and analysts are then obliged to be transparent about their judgment and record their reasoning.

The third obstacle is the threat of greenwashing, at the level of the company and during the analytical procedure. Firms can make bold sustainability pledges that lack the disciplines of operational infrastructure and capital allocation to fulfill. The importance of corporate ESG disclosure should be approached in a similar manner as management earnings guidance that analysts should approach with a critical scepticism. Comparing company disclosures with independent assessments, records of regulatory enforcement, and investigative journalism may assist in uncovering the differences between the proclaimed ESG commitments and performance.

Process Flow 2: ESG Due Diligence in M&A Transactions

| Phase 1 | Phase 2 | Phase 3 | Phase 4 | Phase 5 |

| Pre-LOI Red Flag Screen ESG. | In-depth ESG Due Diligence. | Quantify Contingent Liabilities | Discuss Price Adjustment / Reps and Warranty. | ESG Integration Plan after the Merger. |

The trend of movement is evident, in spite of these challenges. Regulatory requirements such as the Corporate Sustainability Reporting Directive (CSRD), by the European Union, and the International Sustainability Standards Board (ISSB) standards are increasingly harmonising ESG disclosure and creating less data gap and enhanced comparability. With better disclosure quality, analytics infrastructure with business valuation models of ESG will be stronger and more justifiable.

Emerging Trends Shaping the Future of ESG Valuation

The most significant emerging trends in business valuation are those that embed ESG considerations structurally into both market pricing and regulatory requirements, rather than treating them as optional overlays. Climate scenario analysis is shifting towards best practice to regulatory expectations. The Bank of England and the European Central Bank (among other central banks) already have economy-wide climate stress tests done. To corporate finance professionals, this will imply that DCF models constructed without climate scenario inputs will be seen as more and more incomplete, as opposed to being conservative.

The second big trend is the increased use of natural capital accounting and biodiversity measures in valuation. Investors and regulators are starting to apply the ESG lens to areas other than carbon to include water security, land use, impact on biodiversity, and ecosystem dependencies. The Taskforce on Nature-related Financial Disclosures (TNFD), the finalised framework of which was published at the end of 2023, is likely to trigger a third wave of disclosure expectations on industries that have a nature-dependent component, such as agriculture, food and beverage, pharmaceuticals, and infrastructure. Both analysts constituting ESG business valuation models will have to gain proficiency in such measurements in the next decade.

The ESG data sourcing and processing are also starting to be transformed by artificial intelligence and machine learning. Other data sources, such as satellite imagery of land use, natural language processing of regulatory filings, and news flow to detect controversy, and supply chain mapping tools, are empowering analysts to have a more detailed and real-time view of ESG performance than can be obtained through voluntary corporate disclosures. By investing in ESG and sustainable financial training that integrates these analysis tools, professionals will be in a better position to be value-added as the profession changes. The inclusion of ESG in valuation is not a new regulatory fad, but a major redefinition of the process of capital market pricing of long-term risk and opportunity.

Conclusion: Actionable Insights for Finance Professionals

The addition of ESG considerations to valuation models is one of the most significant analytical innovations in corporate finance in the last 10 years. It asks finance professionals to broaden their toolkit – by relying on ESG data vendors, sustainability frameworks, techniques of scenario analysis, and materiality judgments that are specific to the sector – and to be as rigorous and sceptical about any financial analysis as they are about any other analysis.

To people just starting their careers, the best investment that they can make is to enhance their basic skills in financial mechanics and the ESG conceptual map. Knowledge of the impact of carbon pricing on EBITDA margin, governance risk on equity risk premiums and the use of scenario analysis to bound the valuation uncertainty are skills that will appreciate in value as the new trend in business valuation lives on to redefine market expectation and regulation standards.

There are a number of practical measures that can be highlighted that can be taken by professionals who want to develop their ESG valuation skills. To start with, get acquainted with the SASB Materiality Map and TCFD framework. These are the reference points of the industry that have the highest number of mentions by institutional investors and credit committees. Second, perform reconstruction of a DCF model of a publicly listed firm operating in a carbon-intensive industry with explicit ESG modifications, as inputs to which publicly available sustainability reports, and third-party ESG scores should be input. Third, find accredited ESG and sustainable finance training courses with professional organisations, such as the CFA Institute, offers a more stringent introduction to the theory of investment and to the practical analytics. Lastly, keep up to date on regulatory changes: CSRD, ISSB guidelines and TNFD framework are all currently being actively implemented, and awareness of their disclosure requirements will be needed to have the necessary confidence in their analytical capabilities of interpreting company-level ESG data.

What will bring the most value in this changing environment will be professionals who will not identify integrating ESG as a compliance liability, but as an analytical opportunity – as a means of seeing risks that other professionals miss, and as a means of developing valuation models that are more reflective of the whole gamut of factors that can drive long-term corporate performance. The ESG business valuation models do not represent an entirely different field of study as compared to mainstream finance; it is just its logical development.