Business valuation based on revenue is calculated by applying industry valuation multiples to a company’s annual or recurring revenue to estimate its market value. This approach is commonly used for growth-stage businesses and is often compared with the discounted cash flow method of business valuation, asset-based valuation, and earnings multiples. All these are used together to give different views of the value of a company.

What Is Business Valuation Based on Revenue?

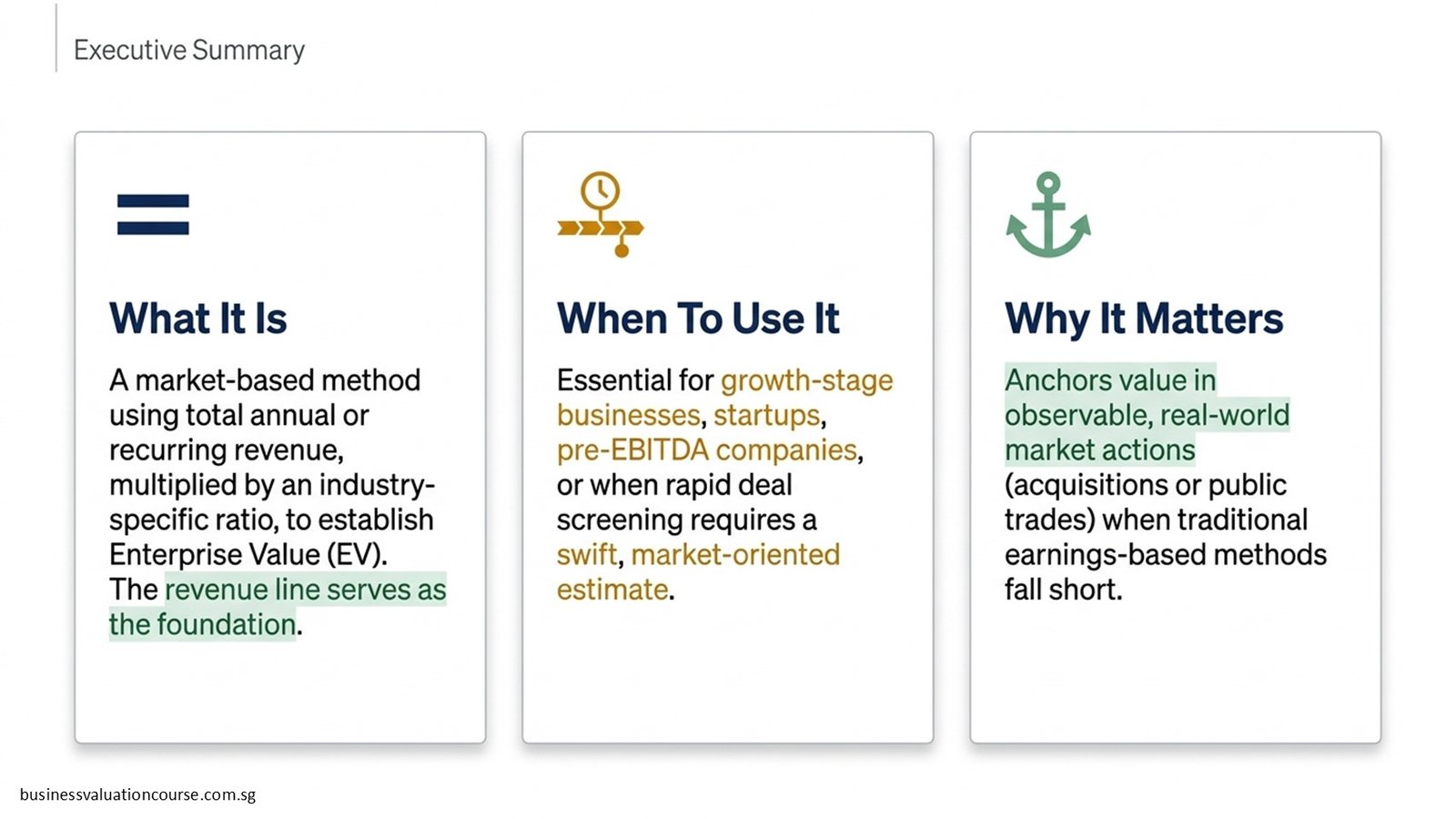

Business valuation is based on the revenue, which is a method of valuing a business using total revenue multiplied by an industry-specific multiple. This is different from merely basing enterprise value on profit or asset value; the revenue line serves as the basis for enterprise value in this approach.

It’s a technique that analysts employ when earnings are irregular, when the companies that are just starting up don’t have positive Earnings Before Interest, Taxes and Depreciation, or when a market-oriented estimate needs to be done quickly. Revenue multiples are based on real market actions, using the transaction of acquisition or an equivalent publicly traded company.

In any good business valuation program, one of the most important skills for students to learn is when to use this approach and how to use it along with other valuation methods.

How Do Analysts Calculate Business Valuation Based on Revenue in Practice?

Revenue-based valuation can be done in a systematic fashion in practice. The first step in analysts’ work is to calculate the company’s total revenue, then choose a multiple, and then use that to estimate the enterprise value.

| Step | Activity | Purpose |

| 1 | Review and normalise revenue | Establish a clean, reliable valuation base |

| 2 | Identify comparable companies or transactions | Benchmark the business against peers |

| 3 | Calculate the EV/Revenue multiple from comparables | Determine market-implied pricing |

| 4 | Adjust for company-specific factors | Reflect risk, growth, and competitive position |

| 5 | Apply the selected multiple to the subject revenue | Calculate the estimated enterprise value |

| 6 | Perform a sanity check against other methods | Validate the result using DCF or earnings multiples |

Normalisation of revenue is an important first step. Analysts add back one-off items, related party transactions, or accounting anomalies that could have an impact on the revenue number to value.

Why Do Revenue Multiples Matter in Business Valuation?

Revenue multiples are the amount of dollars that investors are willing to spend on one dollar of revenue for a business. They act as a shortcut that reflects collective expectations of a company’s growth prospects, risk, and competitive longevity, based on the market.

Revenue multiples, in the context of investment banking, private equity, or corporate finance, is a no-brainer; it’s a vital part of market-based valuation. Multiples can differ across industry sectors, within company size, across growth rates, and depending on the market conditions.

Business valuation training teaches analysts how to analyze multiples, rather than just use them. A high multiple means that the company has had strong recurring revenue; a low multiple might mean that the company has been affected by pricing pressure, customer concentration risk, or falling growth.

How Do Analysts Select Appropriate Revenue Multiples?

One has to choose appropriateness, not just the right multiple. Enterprise value-to-revenue (EV/Revenue) ratios are used by analysts to compare the subject company with a peer group of publicly listed companies or recent private transactions.

Revenue growth rate, gross margin profile, customer retention, business model predictability and market position are key factors impacting multiple selection. An EV/Revenue multiple represents a high number for a Saas firm with 90% gross margins and high retention rates compared to a low margin distribution business.

The professionals who get the structured valuation training gain the capacity to take a look at peer groups, determine median and mean multiples, and make defensible adjustments for differences in company quality.

| Industry / Sector | Typical EV/Revenue Range | Key Multiple Drivers |

| SaaS / Cloud Software | 5x – 15x+ | Recurring revenue, retention, growth rate |

| Technology (hardware) | 1.5x – 4x | Product cycle, margins, R&D intensity |

| Professional Services | 0.5x – 2x | Client concentration, utilisation, brand |

| E-commerce / Retail | 0.3x – 1.5x | Volume, logistics efficiency, margins |

| Healthcare / Medtech | 2x – 6x | Regulatory moat, recurring demand |

| Financial Services | 1x – 3x | Regulatory capital, asset quality, and fee stability |

| Manufacturing | 0.4x – 1.2x | Capacity utilisation, input cost exposure |

The ranges are indicative only. The actual multiples will vary with market timing, deal features, and company results. Static benchmarks should not be used by analysts to validate multiples; they should validate these multiples against a current transaction that is similar to the transaction being analyzed.

What Factors Influence Revenue-Based Valuation Results?

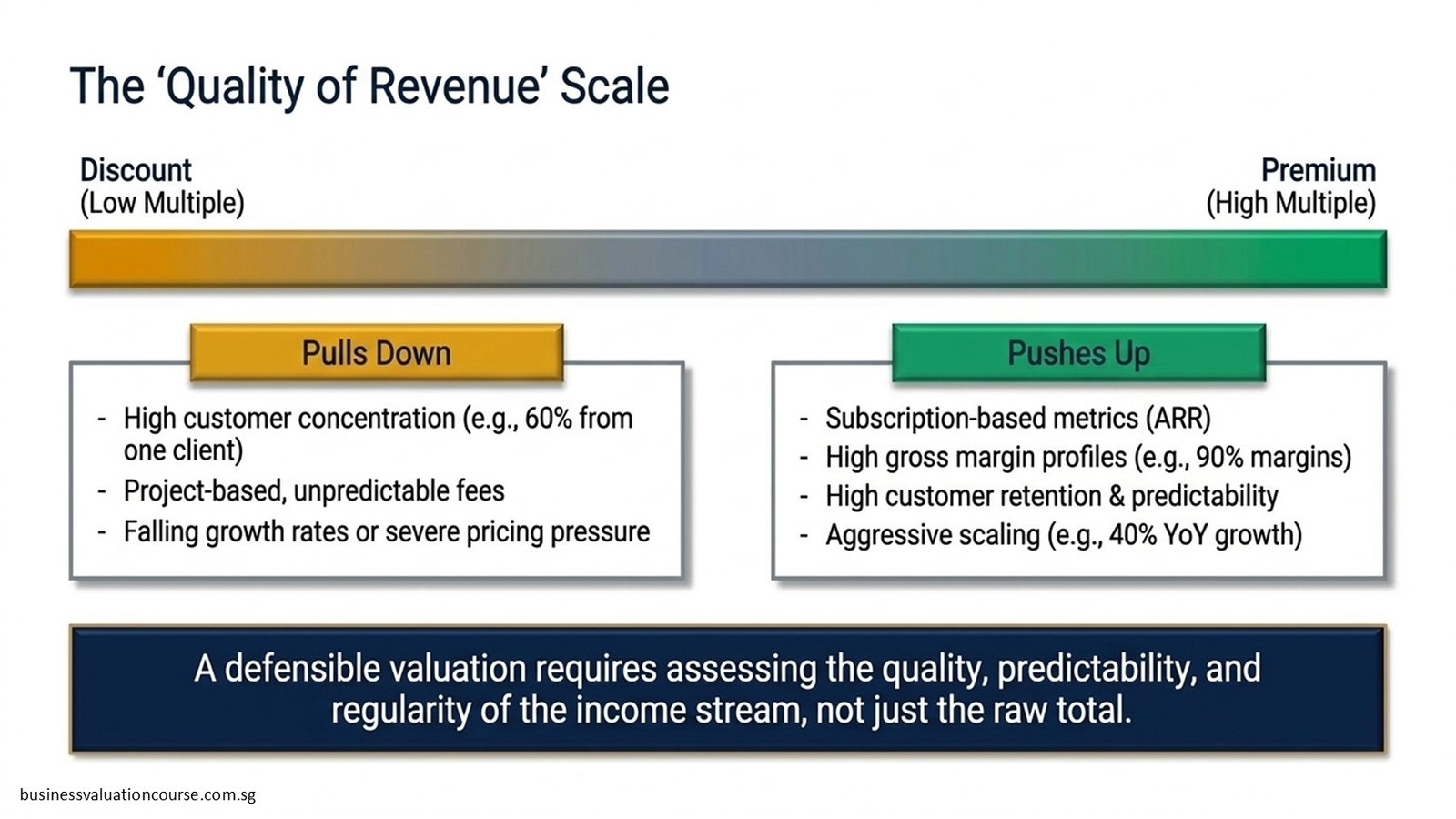

There are a number of qualitative and quantitative determinants for valuation output. A defensible conclusion to the valuation requires an analysis of both the quality of revenue and the overall business environment.

Revenue quality is a measure of the reliability, predictability and regularity of the income stream. Subscription-based revenue is more valuable than project fees. A high level of customer concentration is also a factor, as a business that relies on 60% of sales from one customer is a higher-risk business and is therefore worth a lower multiple.

Prospects for growth are a significant factor. If a company is growing by 40% a year, it can be a profitable company, but it may not be profitable at the moment, so a higher multiple may be justified. However, a company with a solid profit margin and no growth in sales may have a higher worth determined by an earnings approach.

How Do Different Industries Apply Revenue-Based Valuation?

Valuation is not the same for every sector; it is revenue-based. There are conventions within each industry on the approach and what measures are being given a higher premium and how growth is weighed against margin.

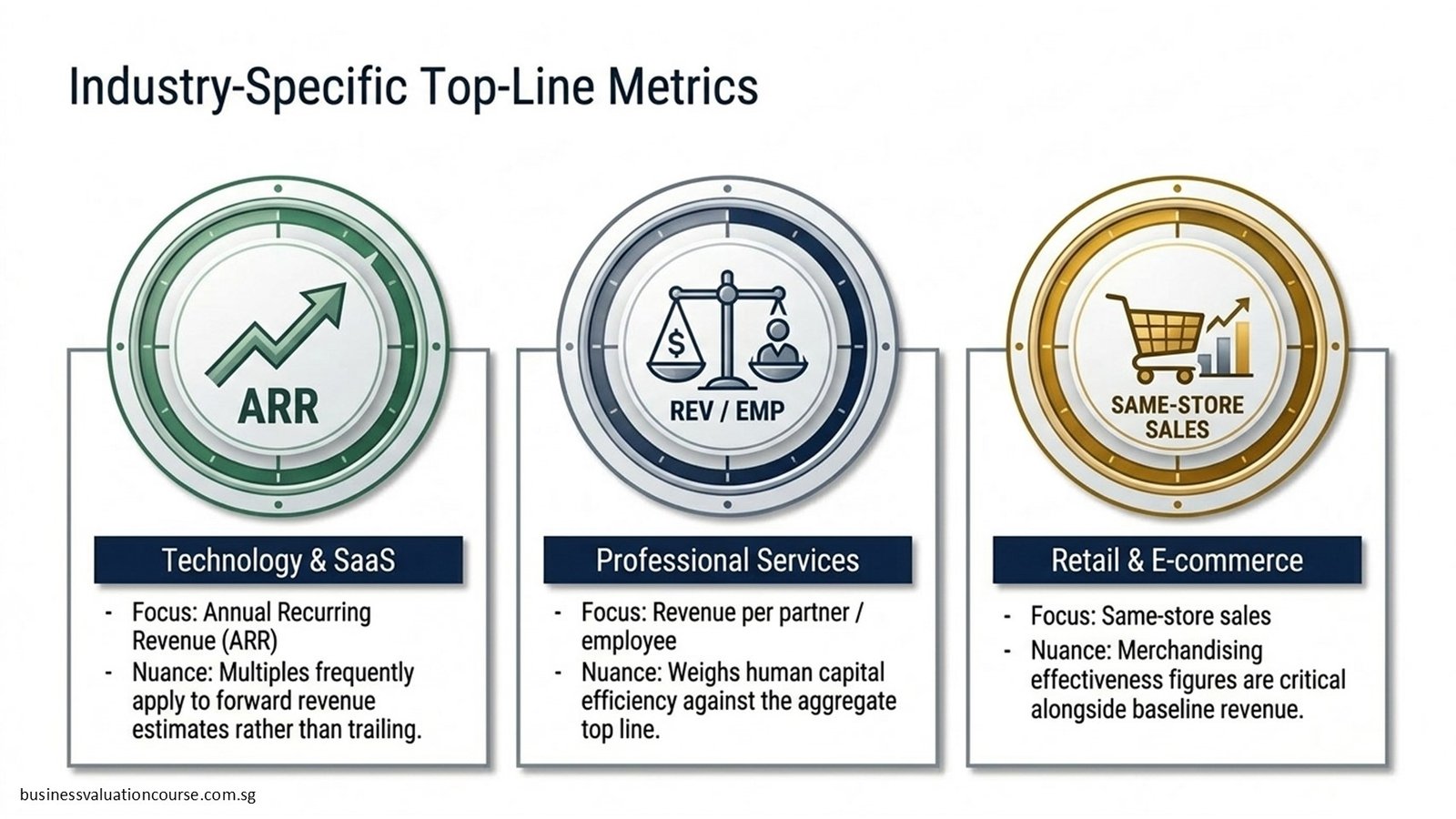

For technology and SaaS, the preferred metric is annual recurring revenue (ARR) and multiples can frequently be forward revenue estimates. Revenue per partner/revenue per employee could be added to the top line in a consulting firm. Analysts pay attention to same-store sales and merchandising effectiveness figures in addition to revenues in retail.

These real-world experiences are introduced to the valuation novice in a systematic and structured course, helping them to become more knowledgeable about and avoid using generic valuation formulas, instead employing local practices and techniques as needed for assignments.

When Should Revenue-Based Valuation Be Used Instead of Other Methods?

Revenue-based valuation is most appropriate when it is not possible or is not reliable to use earnings-based valuation. This includes early-stage companies with negative EBITDA, businesses restructuring to alter their current profitability, and high-growth companies where the value created in the future outweighs the profitability today.

It is also widely used in preliminary deal screening or indicative valuation exercises, where speed is the priority and a ‘ballpark’ valuation may be adequate. In cases of investment decision, M&A transactions, or for regulatory purposes, revenue multiples should be used in conjunction with more rigorous methods for final valuations.

Professional judgment on the scope of the method is one of the skills that is acquired through the method and practice, and is better served by those who are familiar with it.

How Does Revenue-Based Valuation Compare with the Discounted Cash Flow Method of Business Valuation?

Revenue-based valuation and discounted cash flow business valuation are based on different assumptions and have different uses. Once a finance professional is engaged in valuation activities, it is important to comprehend the difference between them.

The DCF method is based on projecting future free cash flows in detail and applying a risk-adjusted discount rate to bring these cash flows back to the current price. It is more analytical but demands more accurate forecasts and assumptions regarding cost structure, capital expenditures and terminal growth. While easier and quicker, revenue multiples rely 100% on the quality of the comparable company set.

| Dimension | Revenue Multiple Method | DCF Method |

| Primary basis | Revenue | Future free cash flows |

| Data required | Comparable transactions and peers | Detailed financial projections |

| Best suited for | Growth companies, early-stage firms | Mature businesses with stable cash flows |

| Complexity | Low to moderate | High |

| Sensitivity to assumptions | Moderate (multiple selection) | High (discount rate, growth rate) |

| Common use case | Quick screening, deal pricing | Investment decisions, fairness opinions |

| Profitability required? | No | Yes (or projected) |

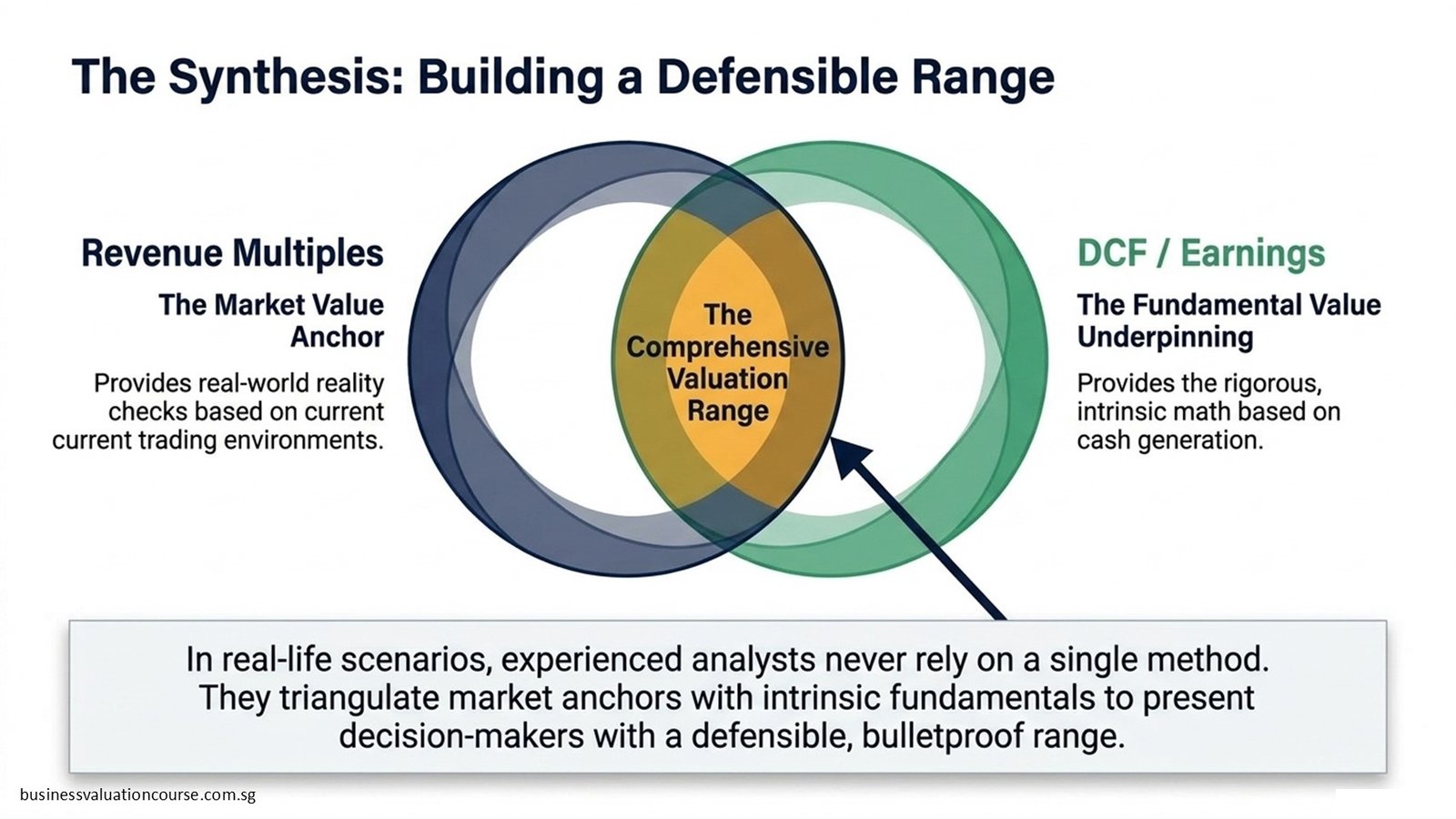

In real-life situations, the two ways of analysis are applied simultaneously by experienced analysts. Revenue multiples offer a market value anchor and the DCF method offers a fundamental value underpinning. If done within a valuation range, it provides the decision makers with a more comprehensive picture.

What Are the Advantages and Limitations of Revenue-Based Valuation?

Revenue-based valuation techniques, like any valuation technique, have some inherent strengths and weaknesses. The method needs to be used responsibly and requires an understanding of both sides.

| Advantages | Limitations |

| Applicable to pre-profit businesses | Ignores cost structure and margins |

| Quick to calculate with market data | Depends heavily on the quality of comparables |

| Anchored in observable market prices | Revenue multiples fluctuate with market cycles |

| Useful for cross-industry screening | May overvalue low-margin or cash-burning businesses |

| Easy to explain to non-technical stakeholders | Less rigorous than DCF for investment-grade analysis |

| Widely accepted in M&A deal structuring | Can be manipulated by revenue recognition choices |

This is no academic awareness, but it’s a real awareness. Revenue multiples can also be very misleading for valuation professionals, such as a fast growth firm with poor unit economics that trades at a premium multiple despite poor fundamentals.

What Skills Do Finance Professionals Need to Perform Revenue-Based Valuation?

The application of revenue-based valuation is a practical and highly technical skill, requiring professional judgment. Analytical work is not just a simple multiplication of a revenue number by a benchmark number.

Professionals should have a good understanding of identifying and screening similar companies, calculating and adjusting EV/Revenue multiples, understanding industry dynamics and how they impact multiple selection, understanding how to normalise revenue numbers for non-recurring items, and triangulating the results across multiple valuation methods.

In addition to the technical expertise, effective valuation practitioners learn to articulate their assumptions and communicate the valuation ranges with clients or management, and also be able to justify their conclusions in front of examination during due diligence or advisory.

How Can Business Valuation Training Improve Practical Valuation Capabilities?

Structured training will rapidly build these skills by combining the theory and practice needed for development that may be lacking in on-the-job training.

A good programme in business valuation includes revenue multiples, DCF modelling, earnings valuation, and asset valuation – providing an all-in-one toolkit for participants. Real-world case studies can help students understand the context of the selection of multiples, the construction of the valuation ranges, and the convergence and divergence of valuation methods.

Professionals seeking to strengthen their practical capabilities can explore programmes such as business valuation based on revenue training courses that cover both market-based approaches and intrinsic valuation methods in an applied setting.

For finance professionals at all career stages — whether entering the field or expanding into advisory roles — structured valuation education provides the rigour and credibility that clients and employers expect.

Conclusion

Market-oriented business valuation using revenue multiples and comparing transactions is widely used and is based on revenue data. It is particularly useful for companies at the growth stage, startups, and when traditional methods of analysis are not feasible or do not yield consistent results.

But revenue-based valuation works best in conjunction with other valuation methods. When earnings multiples or asset-based approaches, or revenue multiples, are added to the discounted cash flow valuation of a business, analysts have a more comprehensive and defensible valuation range.

Knowing the time for each method and interpreting the results in the context of the business or transaction is where the difference lies between the pros and the cons. Judgement is developed by education, practice, and exposure to real valuation assignments.

| Concept | Key Takeaway |

| Revenue multiple method | Estimates value by applying EV/Revenue ratios derived from market comparables |

| Multiple selection | Driven by industry norms, growth rate, margin profile, and revenue quality |

| DCF vs revenue multiples | DCF offers greater rigour; multiples offer speed and market anchoring |

| Appropriate use cases | Pre-profit firms, growth companies, deal screening, and preliminary valuations |

| Professional application | Best deployed alongside DCF and earnings methods for a complete valuation picture |

| Training benefit | Structured programmes develop both analytical skills and professional judgment |

The acquisition of a solid understanding of revenue-based valuation (along with the other primary valuation techniques) is good business for finance professionals, investment analysts, business owners and consultants.