What Is Asset-Based Business Valuation and How Does It Work?

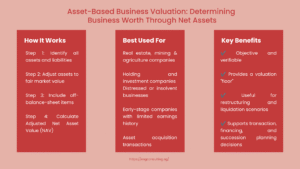

Asset-Based Business Valuation is the process of calculating a company’s value based on its total assets minus total liabilities, resulting in a Net Asset Value (NAV). It is one of the three most common business valuation techniques (along with the income approach and the market approach) and works best when the value of a business is based on what it possesses, not what it generates.

This article shows how the approach works, what it includes, when to use it and how it differs from other approaches to valuation.

What Is Asset-Based Business Valuation?

The asset-based business valuation method can be used to determine the net worth of a business by subtracting the value of all assets from the value of all liabilities. The resulting number, “net asset value” (NAV), is what the shareholders will have theoretically if the assets are all sold and all the debts are paid.

This is based on the accounting equation: Assets = Liabilities + Equity. The accounting of assets in the financial statements, however, is at historical cost, which may be quite different from the market realities. The asset-based approach overcomes this by revaluing the numbers to what they are worth at fair market value or at liquidation value, as appropriate.

There are two primary variants:

- Going concern basis: Assets are priced at the levels they could be obtained at if the business continues.

- Liquidation basis: Basis used in liquidation when the value of the assets is based on amounts they may be realised in a forced or orderly sale.

The basis of valuation will have a significant impact on the final valuation and should be based on the realities of the business.

How Does the Asset-Based Valuation Approach Work?

There are four steps to the business valuation asset approach: step from raw balance sheet data to a restated net asset value, based on current market conditions.

Step 1 — Identify all assets and liabilities. Consider the entire balance sheet – tangible fixed assets, current assets, intangible assets, debt, and obligations.

Step 2 — Adjust to fair market value. Revalue each asset on the balance sheet from historical cost to current market value. Revalue each asset on the balance sheet from historical cost to current market value. Property may have increased in value, and equipment may be worn out quicker than the accounting depreciation schedules.

Step 3 — Identify off-balance-sheet items. Record contingent liabilities, operating leases and internally generated intangible assets that may not be in the books.

Step 4 — Calculate adjusted net asset value. Add up all the assets and deduct all the liabilities restated. The outcome is the adjusted book value (valuation output).

Why Is Asset-Based Valuation Considered One of the Different Business Valuation Methods?

There are three fundamental frameworks that are recognised in professional valuations. For a comprehensive comparison, resources covering different business valuation methods in M&A and IFRS contexts are especially useful. The table below summarises how each approach differs:

| Approach | Core Question | Best Suited For |

| Asset Approach | What is the property of the business after the debts have been paid? | Companies with high asset turnover ratios and companies holding companies, distressed companies. |

| Income Approach | What is the present value of future cash flows? | A business that has a regular income and is successful. |

| Market Approach | What are comparable businesses worth? | The businesses have enough comparable transaction information. |

The asset approach is most theoretically sound if a company’s value is more towards its holdings than its earning power. It is used as a floor valuation, a minimum valuation used to test the income-based and market-based valuations.

What Assets and Liabilities Are Included in an Asset-Based Valuation?

The comprehensive asset-based valuation includes a broad range of the company’s economic assets and liabilities—including those not found on a typical balance sheet.

| Tangible Assets | Intangible Assets | Liabilities |

| Real property (land & buildings) | Trademarks & patents | Bank loans & credit lines |

| Plant, equipment & machinery | Customer lists & databases | Trade payables & accruals |

| Vehicles & fleet | Software & proprietary tech | Long-term debt & leases |

| Inventory & raw materials | Licences & regulatory approvals | Deferred tax liabilities |

| Cash & cash equivalents | Goodwill (in some contexts) | Contingent liabilities |

| Accounts receivable | Non-compete agreements | Pension obligations |

The most difficult assets to value are intangible assets. Intangibles which are developed internally, such as a brand that has been developed over an extended time, may not be recorded in the accounts but could be real value that a buyer would place on the brand. Valuation, if not accounted for as off-balance-sheet items, can be significantly affected by off-balance-sheet liabilities.

What Is the Difference Between Book Value and Fair Market Value?

Book value is the net value of a business as it appears in the books, which is the sales value minus accumulated depreciation, an accounting construct that is not necessarily true in economic fact. The value of an asset in a free market is the price that would be offered if it were sold at arm’s length, without pressure or coercion on either the buyer or seller.

Let’s assume you bought a commercial property for $500,000 15 years ago. The book value, after depreciation, may be $200,000, but the fair market value may be $900,000 in a booming real estate market. The use of book value here would vastly underestimate the value of the business.

The table below highlights the key differences:

| Criterion | Book Value | Fair Market Value |

| Basis | Historical cost less depreciation | Current price in an arm’s length transaction |

| Reflects market conditions? | No | Yes |

| Used in financial statements? | Yes (GAAP/IFRS) | Only on revaluation or acquisition |

| Risk of over/understatement | High — especially for property | Low when supported by appraisal |

| Preferred in valuations? | Rarely | Yes — industry standard |

The book value adjustment removes these distortions and restates each asset — and, if applicable, each liability — to fair market value, and provides a true value of the business.

When Should Businesses Use the Asset-Based Valuation Approach?

Business valuation asset approach is suitable in a scenario in which the value of the business is based on the various assets that the company holds as opposed to the earning potential. The major scenarios are summarized in the following table:

| Business Type | Reason Asset Approach Fits | Valuation Basis |

| Real estate/mining / agriculture | Value lies in physical holdings | Going concern or liquidation |

| Holding & investment companies | No operating earnings to discount | Going concern (NAV) |

| Distressed/insolvent businesses | Focus on recovery for creditors | Liquidation basis |

| Early-stage companies | Limited earnings history | Going concern (adjusted NAV) |

| Asset acquisition transactions | Buyer values specific assets, not business | Fair market value per asset |

In these situations (typically a high-margin professional services business), the income or market approach will tend to be more significant.

How Does Asset-Based Valuation Compare with Income and Market Approaches?

The three valuation methods respond to various basic questions and are appropriate to various business profiles.

The income approach asks: It is appropriate for profitable going concerns that have steady cash flows and can be very sensitive to the assumptions about growth and discount rates.

The market approach asks: It will rely on actual transaction information, and the comparable deals are actually needed — which will not always be easily accessible for private enterprises in niche markets.

The asset approach asks: It can be objective and verifiable but might be underestimated for companies with significant earnings and branding power.

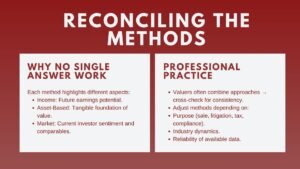

In real life, professional valuations will employ all three methods and balance them. Each is given a weighting according to the business type, the purpose of the valuation and the availability of the data. Businesses that have assets would be more inclined to use the asset approach, while service or tech businesses would be more inclined towards income.

What Are the Advantages and Limitations of the Asset-Based Valuation Approach?

There are definite advantages and limitations to the asset approach. It is important to comprehend both to use it as needed.

| Advantages | Limitations |

| Objective and verifiable – according to balance sheet data | May value a profitable business at less than its true worth |

| Reaches a reasonable minimum price | Intangible assets are assets that cannot be measured in terms of money. |

| Helpful in distressed or wind-down situations. | Off-balance-sheet items are subject to easy oversight. |

| A coherent approach is only available for non-operating entities. | Does not recognise going-concern synergies |

| Adheres to IFRS 3 – purchase price allocation | Assessment of material assets is expensive, and involves an external specialist. |

The bottom line: The asset approach is most likely to be used as a floor value or a key method for asset-based businesses, and least likely to be used as a stand-alone method for income-based businesses.

How Can Companies Improve the Accuracy of Asset-Based Valuation?

There are a few steps that can be taken to ensure that an asset-based valuation is accurate and defensible.

Engage qualified appraisers. Specialized plant, if any, and property should be appraised by independent, certified appraisers. Material risk is introduced by using book values and/or estimates based on internal information.

Audit intangible assets. Carry out a systematic review (including non-balance sheet assets). An IP audit can reveal trademarks, software and licences which have significant economic significance but which are not evident in financial records.

Quantify contingent liabilities. Seek legal advice to evaluate existing and future claims and conduct extensive warranty analysis and tax analysis.

Use current market data. Fair value adjustments should be based on recent observable information: comparable property sales, equipment quotes or quoted market prices, rather than on internal information.

Document assumptions clearly. For each adjustment, a sound explanation and justification should be provided. This is crucial for trust in transactions, disputes, and regulatory evaluations.

Reconcile with other methods. If there is a significant difference from the income-based or market-based results, it is an indication that something has gone wrong with a particular asset, an unrecorded liability, or the assumptions of the earnings. Any significant difference between income-based conclusions and market-based conclusions is an indication that something is wrong with a particular asset, there is a liability that hasn’t been recorded, or the assumptions of the earnings is incorrect, all of which should be investigated.

Conclusion: What Is Asset-Based Business Valuation and How Does It Work?

Asset-Based Business Valuation is a systematic and clear approach to apply to measure the value of a business based on its assets and liabilities. The process of adjusting the figures in the balance sheet to fair market value results in an adjusted book value that provides a more true and fair picture of the economy as opposed to accounting convention.

The asset approach is the most powerful method to business valuation for asset-intensive businesses, holding companies, and businesses facing distress. It offers a solid base for negotiations and facts for transactions, litigation, and financial reporting.

It is best used in conjunction with — not in place of — the income and market approaches to the business valuation asset approach. All three are reconciled to give the most defensible and complete valuation conclusion.

For business owners, investors and finance professionals, the lesson to take away is: don’t take your financial statements at face value. This is because a well-done asset-based valuation, using independent appraisals for assets and a comprehensive analysis of on and off-balance-sheet assets and liabilities, often offers a materially different — and more accurate — view of the value of a business. Knowing the basis of your assets is a key first step in many situations: a sale, getting financing, succession planning, etc.