Business valuation courses cover methods for assessing the liquidation value of a business by evaluating the value of assets during liquidation, comparing the results with the income approach, and applying structured valuation methods used in restructuring, financial reporting, and transaction analysis. Learners build practical skills through case-based exercises and guided financial analysis.

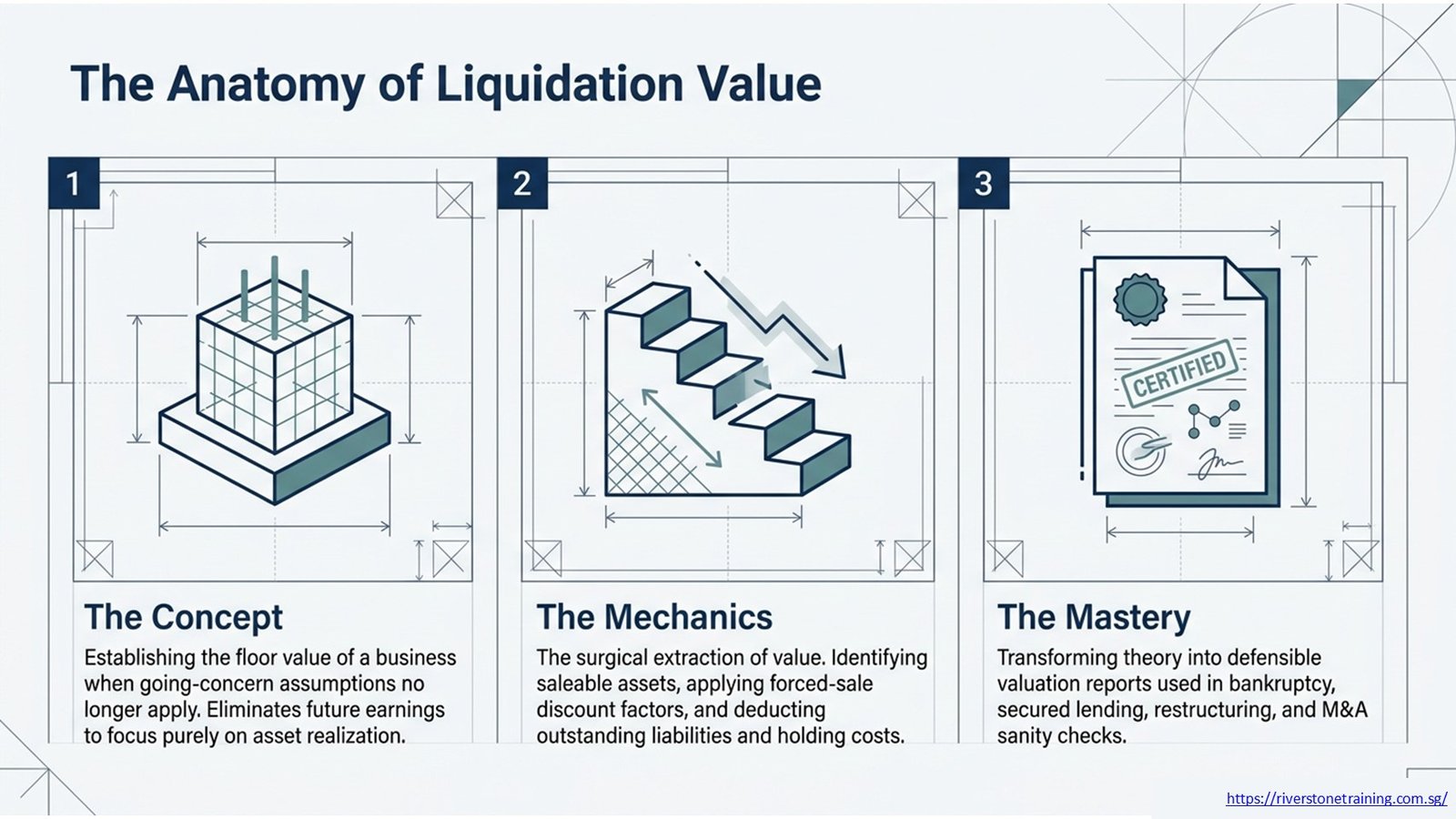

What Is Liquidation Value in Business Valuation?

The approximate value of a business after its assets are sold and its debts are paid back, usually within a specific period of time. It shows the value of assets that have been acquired and are usable but not the current earning power of the company.

In practice, the liquidation value of a business is calculated by the analysts by determining the saleable assets, estimating the likely sale proceeds, and deducting the outstanding liabilities and the liquidation costs from these figures. It is commonly employed in situations where a company is being wound up, turned into a liquidation, or going through asset sales. Liquidation value is one of the more conservative of the outputs from a valuation engagement as it eliminates assumptions about future operations.

Why Is Liquidation Value Important in Business Valuation?

Liquidation value is important because it is a good indicator of a business’s floor value, which is valid where going-concern assumptions are no longer applicable. It is used by lenders, insolvency practitioners and auditors to determine minimum value in distressed scenarios. Otherwise, stakeholders would not have a clear reference for financial outcomes in the worst-case scenario.

Other valuation outputs can be better understood with a view to the value of the business in liquidation. For instance, the liquidation value versus income approach valuation can reveal how much value is in the business, as opposed to the assets. This comparison can be a major issue when discussing restructuring plans with creditors.

How Do Business Valuation Courses Teach Liquidation Value Assessment?

Business valuation courses are taught in structured modules that include asset identification, estimation of the value of the assets that are likely to be realised, the deduction of liabilities, and the report. Students work through examples of distressed businesses, businesses that have a lot of assets, and restructuring situations. The teacher usually demonstrates examples of how to use the framework they have just discussed, and then has the students try independent problems.

Hands-on financial modeling exercises are usually incorporated into the training, such as preparing liquidation schedules and adding discount factors for forced sales, and then comparing the results with the income and market approach valuation results to help develop professional judgment. Sometimes draft valuation reports are sent to peers for review to mock the process of peer review that is experienced by professionals during actual valuation engagements.

How Is Liquidation Value Different From Fair Market Value?

Fair market value is determined by the assumption of a willing buyer and a willing seller and sufficient marketing time, whereas liquidation value places a pressure sale and a willing seller on the willing buyer. This difference in values usually leads to a liquidation value being lower than fair market value, particularly for illiquid assets or specialized assets.

It is an important point students are taught when learning about courses because an analyst has to choose the appropriate value standard for a particular engagement. In a distressed sale environment or in the event of a healthy ongoing business, use of fair market value or liquidation value may lead to materially inaccurate conclusions that negatively impact the credibility of the entire valuation report.

When Should Analysts Use Liquidation Value?

Liquidation value is suitable if a business is winding up and/or insolvent, or when creditors wish to evaluate the recovery of collateral in the event of worst-case scenarios. It is also applied in certain financial reporting contexts where the determination of the assets held for sale and disclosure of the realizable value is required to be accurate.

During mergers and acquisitions, analysts use liquidation value as a sanity check to make sure that a proposed transaction price isn’t lower than the price that they would expect that they could generate from the sale of the assets. This mechanism is to protect the sellers from a lower valuation of the underlying assets in the sellers’ offer.

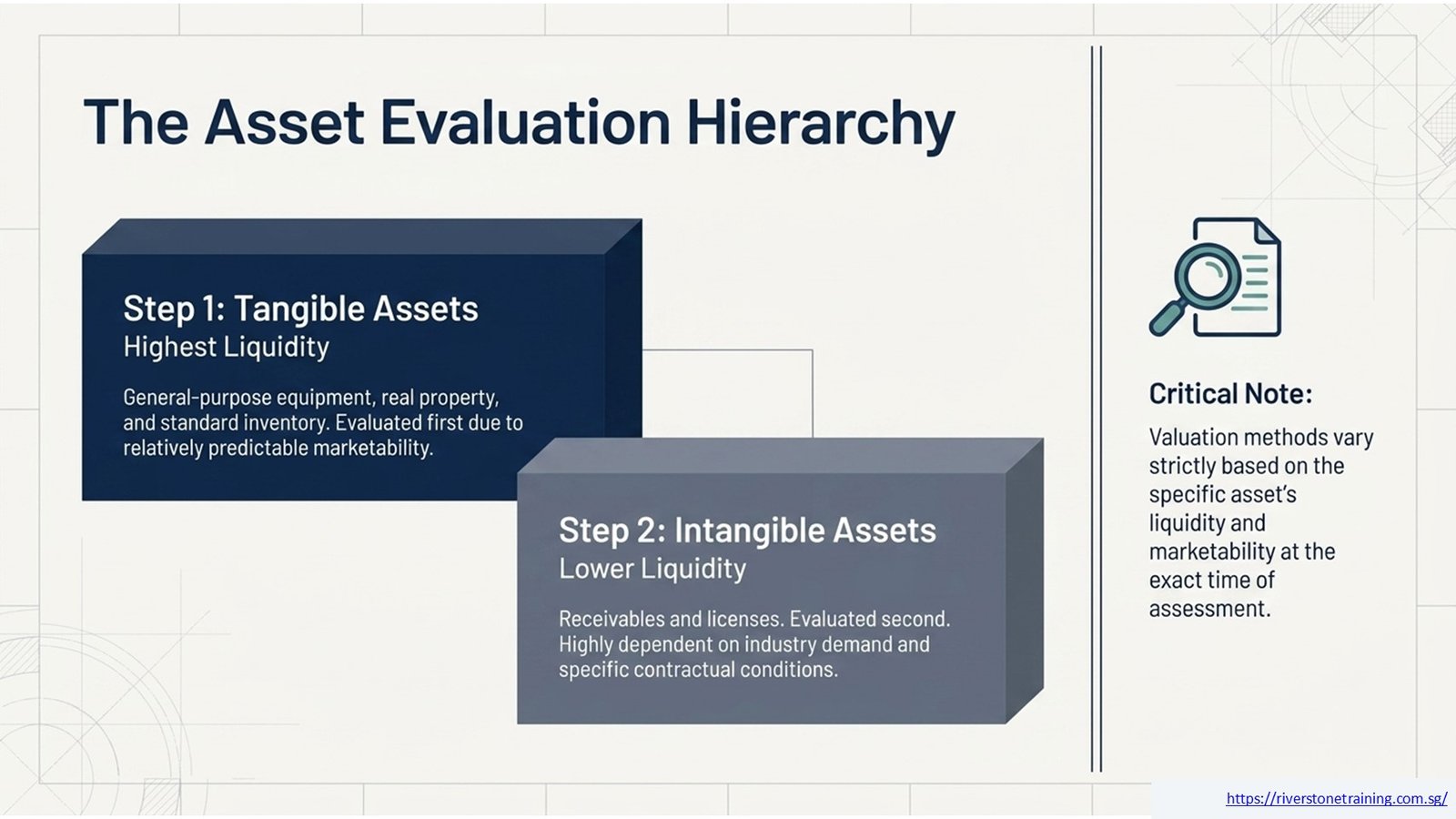

How Are Business Assets Evaluated During Liquidation?

The order of asset evaluation in a liquidation is normally based on the number of tangible assets (e.g., equipment, inventory, property) and then the number of intangible assets (e.g., receivables, licenses). There are different methods of valuation for different assets depending on the liquidity of the asset and marketability.

Analysts then estimate the realised proceeds based on discounts reflecting conditions of forced sale, holding costs and time constraints, and then deduct liabilities and liquidation costs to achieve net liquidation value. Many courses take time to explain to students why they are making the discount assumption, instead of giving them a percentage.

What Factors Affect Liquidation Value?

Some of the important aspects are the state of the assets, marketability, demand in the industry, sales time, and the nature of the “orderly” or “forced” nature of the liquidation. The size of the share of a specialized asset or an illiquid asset that is recovered in book value is generally less than the amount of the recovered share of general-purpose equipment or the amount of the recovered share of inventory.

There are also liquidation costs, secured creditor claims, and legal and contractual costs that further diminish the net liquidation value that business owners and creditors might expect to recover. Courses prepare learners to systematically consider these deductions, not afterthoughts.

How Does the Income Approach Compare With Liquidation Value?

Income approach valuation values the business based upon the present values of the projected future cash flows of the business, instead of the proceeds of sale of the assets. It is therefore quite different from liquidation value, which does not consider any future earnings at all. Learn more about how these methods relate in this income approach valuation resource.

In the valuation process, both of these figures are usually compared during the valuation engagements; a significant difference between the two would indicate that the value of the business is mainly based on its future operations rather than the value of its assets at the time of liquidation. This gap is used to sustain a continuing operation rather than to close the plant, and this is often used to justify continued operation when options for plant closure are being considered.

How Does the Market Approach Support Business Valuation?

Market Approach Valuation is a method of valuing a business by applying multiples (such as revenue or EBITDA) to other businesses that have recently sold and/or are publicly traded. It is the source of market-based evidence to complement income and liquidation evidence as detailed in the following market approach valuation reference.

Courses instruct students on how to identify the appropriate comparable companies, how to adjust for size and risk differences, and how to use the valuation multiples from the market approach appropriately, not compromising the credibility of the course results when compared to those found in the liquidation and income approach. Learners also learn how to access and verify similar transaction information from public filings and industry databases.

How Do Analysts Select the Appropriate Valuation Method?

The selection of the method will depend on the purpose of the valuation, the nature of the business, and assumptions for the engagement. Liquidation value may be appropriate if a business has a heavy asset portfolio, whereas a service-oriented business may need to focus more on income approach valuation.

Business valuation courses may explain a decision framework that is structured for valuing a business, which includes an understanding of several approaches and, when applicable, reconciling the conclusions of value to a conclusion that is supported. This reconciliation step is frequently the most difficult of a valuation engagement, and may require clear documentation of judgment calls.

What Financial Analysis Skills Are Developed in Business Valuation Courses?

Students learn to read financial statements, adjust for non-operating items, create discounted cash flow models and conduct comparable company analysis. All valuation techniques, such as liquidation valuations, are based on these skills.

Courses also boost report-writing and communication abilities, as valuation conclusions must be clearly documented and defensible to transaction counterparties, lenders, courts, or auditors. Students learn to communicate data to technical and non-technical audiences effectively.

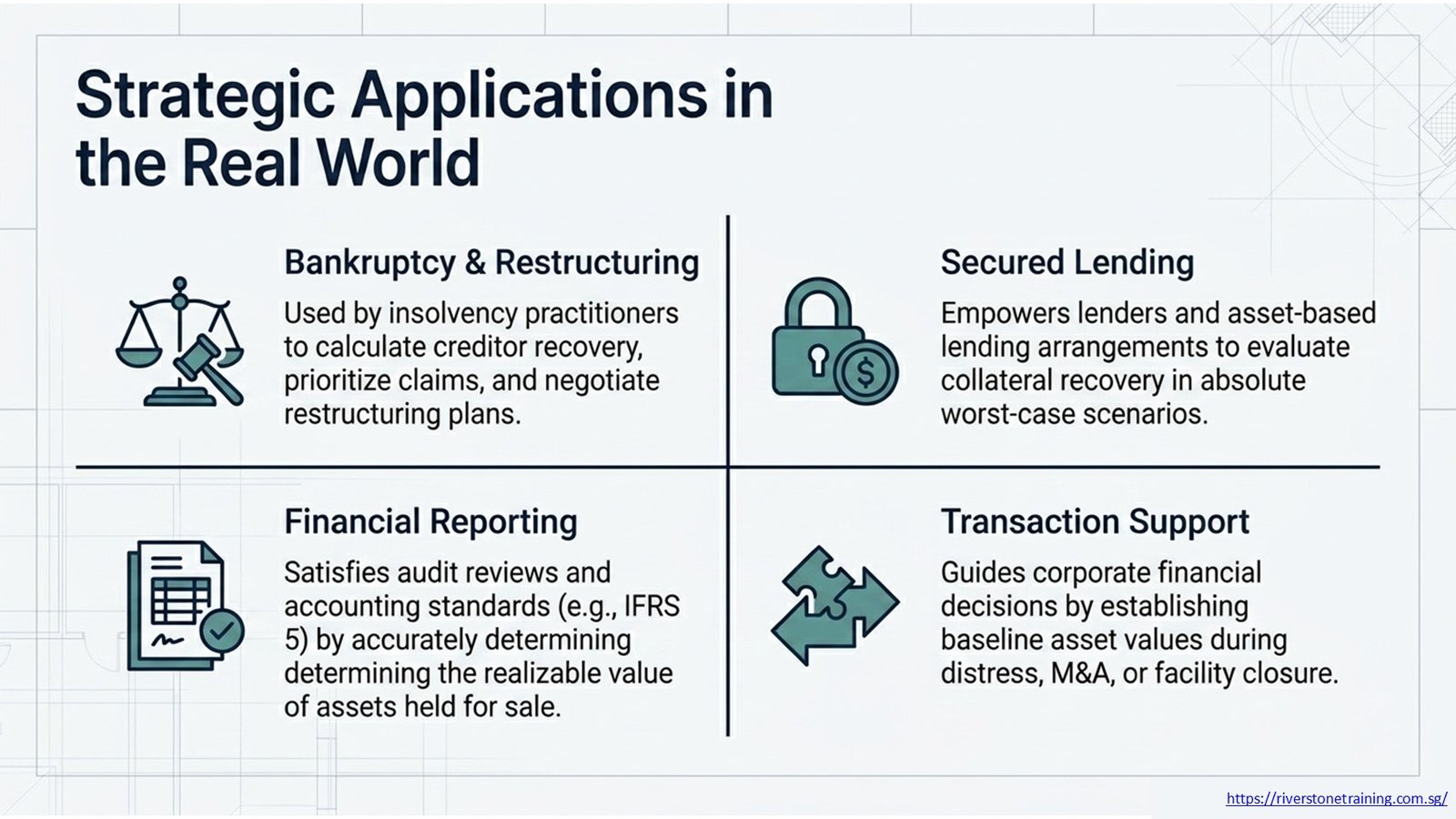

How Are Liquidation Value Assessments Applied in Real Business Situations?

The liquidation value assessment assists in decisions, such as in bankruptcy proceedings, secured lending, business restructuring, and asset-based lending arrangements. These numbers are used by insolvency practitioners to calculate creditor recovery and to prioritise claims.

They also play an important role in financial reporting scenarios, such as determining the value of assets held for sale, which requires accurate estimation of the assets’ realizable value, in order to meet the accounting standards and to satisfy audit review. Supporting workpapers are often called for by auditors to support these estimates when reviewing the year-end.

What Common Mistakes Should Be Avoided in Liquidation Valuation?

Common errors involve applying the fair market value assumptions in a forced liquidation context, not accounting for liquidation costs, or not differentiating between the liquidation timing in an orderly and forced liquidation, resulting in materially different outcomes.

The analysts are also cautioned against relying on out-of-date asset records and not taking secured creditor priority into account, which may be inappropriate or misleading to those who rely on the report. The frequent re-booking of asset registers can help stop these errors from making it to a final report.

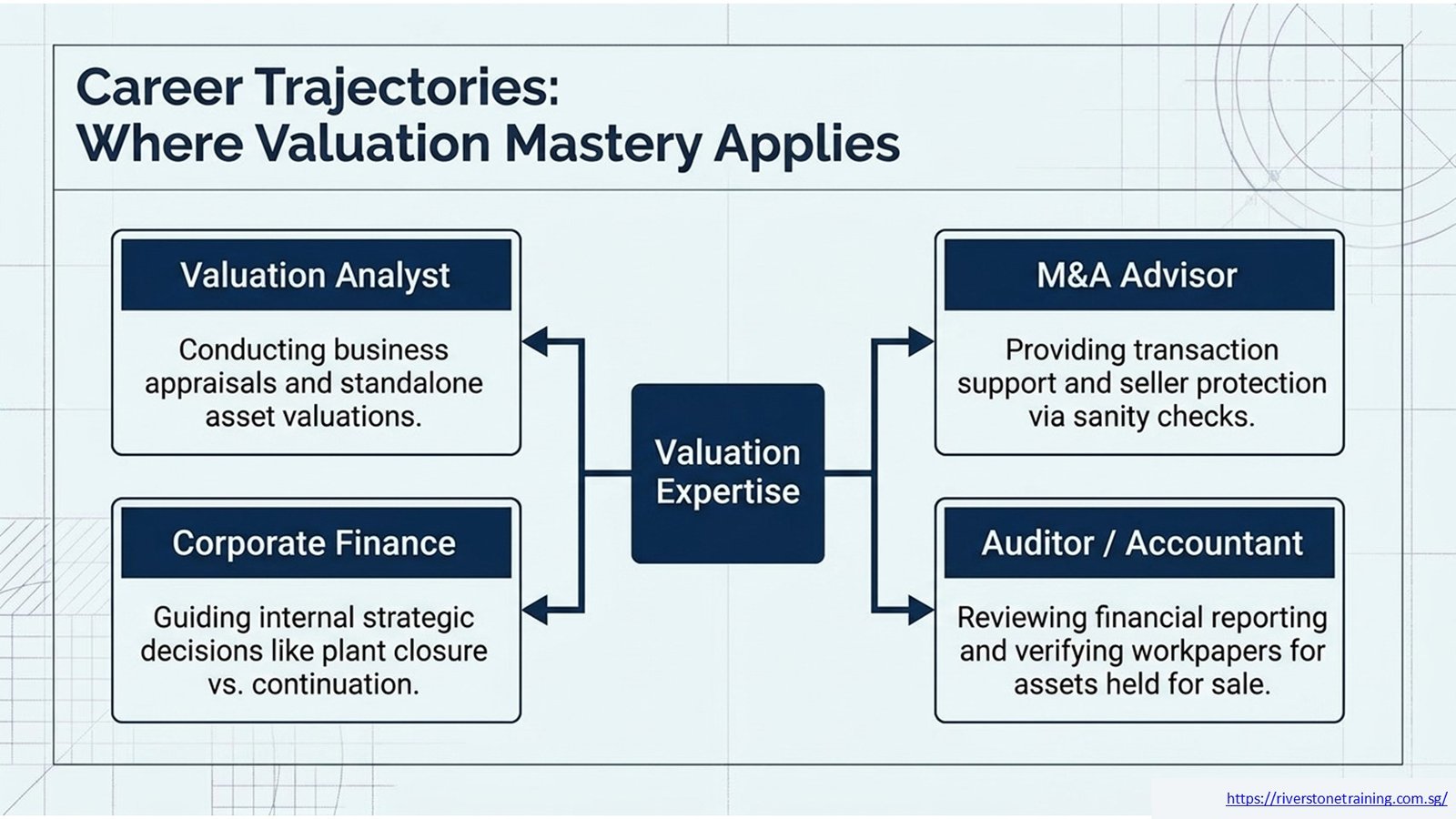

How Can Business Valuation Skills Support Career Development?

Valuation skills are transferable to career opportunities in corporate finance, M&A advisory, auditing and investment analysis. Experts with the confidence to apply the liquidation, income and market approach are more likely to be in a position to provide advisory and decision support services.

Properly preparing a valuation report that is grounded in credible theory, supported with evidence, and defensible in the event of a transaction, dispute, or regulatory review is growing in significance to employers. This is a kind of power that can sometimes set a junior analyst apart from analysts who are given the green light to deal with independent client work.

Why Is Practical Valuation Training Important for Finance Professionals?

Practical training connects the theory of valuation to the practical world, allowing professionals to make the necessary judgments when relevant data is incomplete or assumptions need to be supported. This preparation means that professionals will have a shorter learning curve when transitioning from classroom exercises to client sessions.

Business valuation courses that focus on case studies and hands-on modeling teach students how to handle liquidation value, income approach valuation, and market approach valuation confidently in a variety of business settings.

Business Valuation Methods Comparison

| Valuation Method | Best Used For |

| Liquidation Value | Business closure or distressed assets |

| Income Approach | Future earning potential |

| Market Approach | Comparable company valuation |

| Asset-Based Approach | Asset-intensive businesses |

Liquidation Value Assessment Process

| Step | Purpose |

| Identify Assets | Determine assets to value |

| Estimate Realizable Value | Assess expected sale proceeds |

| Deduct Liabilities | Calculate net liquidation value |

| Prepare Valuation Report | Support business decisions |

Income Approach vs Market Approach vs Liquidation Value

| Method | Primary Focus | Strength |

| Liquidation Value | Asset realization | Conservative valuation |

| Income Approach | Future cash flows | Earnings potential |

| Market Approach | Market comparisons | Current market evidence |

Career Applications of Business Valuation Skills

| Role | Valuation Application |

| Valuation Analyst | Business appraisals |

| M&A Advisor | Transaction support |

| Corporate Finance Professional | Strategic decisions |

| Auditor | Financial reporting reviews |

Conclusion: Building Practical Valuation Expertise

Business valuation courses provide a body of knowledge for valuation that includes liquidation value assessment as well as the income approach and the market approach of valuation and instruct students on how to reconcile the disparities of the various approaches to reach a defensible conclusion.

Real-world, case-based training enables professionals to conduct reliable valuations, assist with financial reporting obligations, and guide corporate financial and investment decisions. Structured, hands-on business valuation training fosters the development of comprehensive expertise and gives business analysts and finance professionals the confidence to work on business valuation engagements.